Essentially, the pendulum swings between a humane goal of bringing these poor victims inside, out of the weather, on the one hand, and getting them out of those snake pits so they can enjoy the benefits of being part of the community, on the other. Every couple of decades, the disadvantages of one approach attract attention, and public opinion demands the opposite. Even the era of effective treatment, which began with Thorazine in 1960, has not relieved the central difficulty, because these people often or usually rebel and stop taking their pills; it is not clear that forcing them to take pills is any greater denial of liberty than forcing them to live in a small room. In 2006 and for the prior five years, a grizzly, disheveled old man who talks to himself has pulled old cardboard around him and slept on the steam grate across the street from the Pennsylvania Hospital. Occasionally, someone summons a passing patrol car which sometimes does and sometimes does not, haul him away.

In March 1765, a remarkably neat and tidy sailor was admitted to the Hospital as insane, and was kept among the other insane patients in the basement rooms. He wandered out, however, and was chased around until he took refuge in the glass cupola that still adorns the roof of the East wing, facing Eighth Street. It was obvious that he would soon have to come down to eat, but the Quakers who ran the hospital at that time would have none of it; they didn't starve their patients. So a mattress was passed up to him, and regular meals. Nothing much could be done about the cold, which must have been pretty severe, but the patient was allowed to remain in the cupola until 1774 when he died. Nine years of room service in the cupola.

For fifty years after that, a subacute psychiatric unit was maintained at 49th and Market, but ultimately the Federal Government found a smokescreen of confusion, sufficient to hide the awkward political backlash. One by one, the huge human warehouses at Byberry, Philadelphia General Hospital, Bellevue in New York and similar places, went out of business. The public wouldn't stand for "snake pits", even Medicare couldn't afford to put millions of insane people into luxury hotels like 49th and Market. And even though there were a few hundred or even a few thousand families that could afford to pay for humane domiciliary care, they had to be sacrificed. A government medical system, essentially run as a political pork barrel, can not afford to permit the continued existence of a visible rebuke by a two-class system.

So, now we're giving these people the benefit of integration into community life, right?

|

|

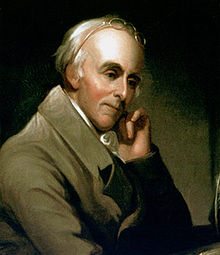

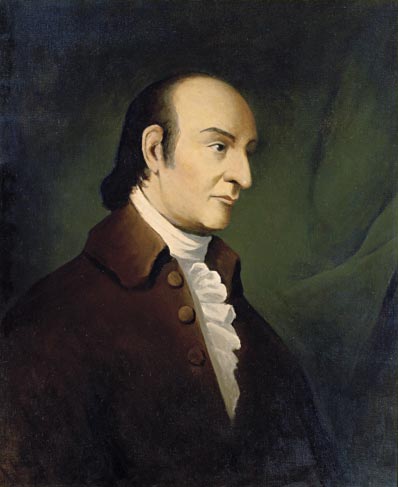

Benjamin Franklin

|

The Last Will and Testament of Benjamin Franklin

I, Benjamin Franklin, of Philadelphia, printer, late Minister Plenipotentiary from the United States of America to the Court of France, now President of the State of Pennsylvania, do make and declare my last will and testament as follows:

|

|

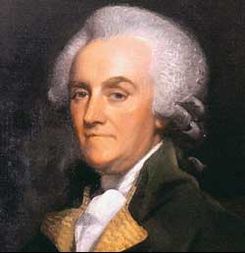

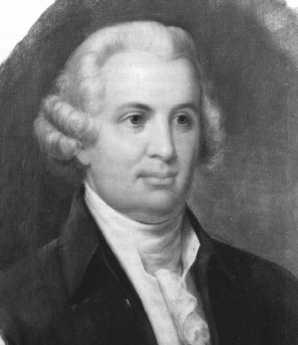

William Franklin

|

To my son, William Franklin, late Governor of the Jerseys, I give and devise all the lands I hold or have a right to, in the province of Nova Scotia, to hold to him, his heirs, and assigns forever. I also give to him all my books and papers, which he has in his possession, and all debts standing against him on my account books, willing that no payment for, nor restitution of, the same be required of him, by my executors. The part he acted against me in the late war, which is of public notoriety, will account for my leaving him no more of an estate he endeavored to deprive me of.

Having since my return from France demolished the three houses in Market Street, between Third and Fourth Streets, fronting my dwelling-house, and erected two new and larger ones on the ground, and having also erected another house on the lot which formerly was the passage to my dwelling, and also a printing-office between my dwelling and the front houses; now I do give and devise my said dwelling-house, wherein I now live, my said three new houses, my printing- office and the lots of ground thereto belonging; also my small lot and house in Sixth Street, which I bought off the widow Henmarsh; also my pasture-ground which I have in Hickory Lane, with the buildings thereon; also my house and lot on the North side of Market Street, now occupied by Mary Jacobs, together with two houses and lots behind the same, and fronting on Pewter-Platter Alley; also my lot of ground in Arch Street, opposite the church-burying ground, with the buildings thereon erected; also all my silver plate, pictures, and household goods, of every kind, now in my said dwelling-place, to my daughter, Sarah Bache, and to her husband, Richard Bache, to hold to them for and during their natural lives, and the life of the longest liver of them, and from and after the decease of the survivor of them, I do give, devise, and bequeath to all children already born, or to be born of my said daughter, and to their heirs and assigns forever, as tenants in common, and not as joint tenants.

And, if any or either of them shall happen to die under age, and without issue, the part and share of him, her, or them, so dying, shall go to and be equally divided among the survivors or survivor of them. But my intention is, that, if any or either of them should happen to die under age, leaving issue, such issue shall inherit the part and share that would have passed to his, her, or their parent, had he, she, or they were living.

And, as some of my said devisees may, at the death of the survivor of their father or mother, be of age, and others of them underage, so as that all of them may not be of capacity to make division, I in that case request and authorize the judges of the Supreme Court of Judicature of Pennsylvania for the time being, or any three of them, not personally interested, to appoint by writing, under their hands and seals, three honest, intelligent, impartial men to make the said division, and to assign and allot to each of my devisees their respective share, which division, so made and committed to writing under the hands and seals of the said three men, or any two of them, and confirmed by the said judges, I do hereby declare shall be binding on, and conclusive between the said devisees.

All the lands near the Ohio, and the lots near the centre of Philadelphia, which I lately purchased of the State, I give to my son-in-law, Richard Bache, his heirs and assigns forever; I also give him the bond I have against him, of two thousand and one hundred and seventy-two pounds, five shillings, together with the interest that shall or may accrue thereon, and direct the same to be delivered up to him by my executors, canceled, requesting that, in consideration thereof, he would immediately after my decease manumit and set free his Negro man Bob. I leave to him, also, the money due to me from the State of Virginia for types. I also give to him the bond of William Goddard and his sister, and the counter bond of the late Robert Grace, and the bond and judgment of Francis Childs, if not recovered before my decease, or any other bonds, except the bond due from ----- Killian, of Delaware State, which I give to my grandson, Benjamin Franklin Bache. I also discharge him, my said son-in-law, from all claim and rent of money due to me, on book account or otherwise. I also give him all my musical instruments.

|

|

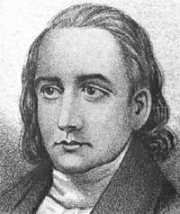

Sarah Bache

|

The king of France's picture, set with four hundred and eight diamonds, I give to my daughter, Sarah Bache, requesting , however, that she would not form any of those diamonds into ornaments either for herself or daughters, and thereby introduce or countenance the expensive, vain, and useless fashion of wearing jewels in this country; and those immediately connected with the picture may be preserved with the same.

I give and devise to my dear sister, Jane Mecom, a house and lot I have in Unity Street, Boston, nor or late under the care of Mr. Jonathan Williams, to her and to her heirs and assigns forever. I also give her the yearly sum of fifty pounds sterling, during life, to commence at my death, and to be paid to her annually out of the interests or dividends arising on twelve shares which I have since my arrival at Philadelphia purchased in the Bank of North America, and, at her decease, I give the said twelve shares in the bank to my daughter, Sarah Bache, and her husband, Richard Bache. But it is my express will and desire that, after the payment of the above fifty pounds sterling annually to my said sister, my said daughter be allowed to apply the residue of the interest or dividends on those shares to her sole and separate use, during the life of my said sister, and afterwards the whole of the interest or dividends thereof as her private pocket money.

I give the right I have to take up to three thousand acres of land in the State of Georgia, granted to me by the government of that State, to my grandson, William Temple Franklin, his heirs and assigns forever. I also give to my grandson, William Temple Franklin, the bond and judgment I have against him of four thousand pounds sterling, my right to the same to cease upon the day of his marriage; and if he dies unmarried, my will is, that the same be recovered and divided among my other grandchildren, the children of my daughter, Sarah Bache, in such manner and form as I have herein before given to them the other parts of my estate.

The philosophical instruments I have in Philadelphia I give to my ingenious friend, Francis Hopkinson.

To the children, grandchildren, and great-grandchildren of my brother, Samuel Franklin, that may be living at the time of my decease, I give fifty pounds sterling, to be equally divided among them. To the children, grandchildren, and great-grandchildren of my sister, Anne Harris, that may be living at the time of my decease, I give fifty pounds sterling to be equally divided among them. To the children, grandchildren, and great-grandchildren of my brother James Franklin, that may be living at the time of my decease, I give fifty pounds sterling to be equally divided among them. To the children, grandchildren, and great-grandchildren of my sister, Sarah Davenport, that may be living at the time of my decease, I give fifty pounds sterling to be equally divided among them. To the children, grandchildren, and great-grandchildren of my sister, Lydia Scott, that may be living at the time of my decease, I give fifty pounds sterling to be equally divided among them. To the children, grandchildren, and great-grandchildren of my sister, Jane Mecom, that may be living at the time of my decease, I give fifty pounds sterling to be equally divided among them.

I give to my grandson, Benjamin Franklin Bache, all the types and printing materials, which I now have in Philadelphia, with the complete letter foundry, which, in the whole, I suppose to be worth near one thousand pounds; but if he should die under age, then I do order the same to be sold by my executors, the survivors or survivor of them, and the money be equally divided among all the rest of my said daughter's children, or their representatives, each one on coming of age to take his or her share, and the children of such of them as may die under age to represent and to take the share and proportion of, the parent so dying, each one to receive his or her part of such share as they come of age.

With regard to my books, those I had in France and those I left in Philadelphia, is now assembled together here, and a catalog made of them, it is my intention to dispose of them as follows: My "History of the Academy of Sciences," in sixty or seventy volumes quarto, I give to the Philosophical Society of Philadelphia, of which I have the honor to be President. My collection in a folio of "Les Arts et les Metiers," I give to the American Philosophical Society, established in New England, of which I am a member. My quarto edition of the same, "Arts et Metiers," I give to the Library Company of Philadelphia. Such and so many of my books as I shall mark on my said catalog with the name of my grandson, Benjamin Franklin Bache, I do hereby give to him; and such and so many of my books as I shall mark on the said catalog with the name of my grandson, William Bache, I do hereby give to him; and such as shall be marked with the name of Jonathan Williams, I hereby give to my cousin of that name. The residue and remainder of all my books, manuscripts, and papers, I do give to my grandson, William Temple Franklin. My share in the Library Company of Philadelphia, I give to my grandson, Benjamin Franklin Bache, confiding that he will permit his brothers and sisters to share in the use of it.

I was born in Boston, New England, and owe my first instructions in literature to the free grammar schools established there. I, therefore, give one hundred pounds sterling to my executors, to be by them, the survivors or survivor of them, paid over to the managers or directors of the free schools in my native town of Boston, to be by them, or by those person or persons, who shall have the superintendence and management of the said schools, put out to interest, and so continued at interest forever, which interest annually shall be laid out in silver medals, and given as honorary rewards annually by the directors of the said free schools belonging to the said town, in such manner as to the discretion of the selectmen of the said town shall seem meet.

Out of the salary that may remain due to me as President of the State, I do give the sum of two thousand pounds sterling to my executors, to be by them, the survivors or survivor of them, paid over to such person or persons as the legislature of this State by an act of Assembly shall appoint to receive the same in trust, to be employed for making the river Schuylkill navigable.

And what money of mine shall, at the time of my decease, remain in the hands of my bankers, Messrs. Ferdinand Grand and Son, at Paris, or Messrs. Smith, Wright, and Gray, of London, I will that, after my debts are paid and deducted, with the money legacies of this my will, the same be divided into four equal parts, two of which I give to my dear daughter, Sarah Bache, one to her son Benjamin, and one to my grandson, William Temple Franklin.

During the number of years I was in business as a stationer, printer, and postmaster, a great many small sums became due for books, advertisements, postage of letters, and other matters, which were not collected when, in 1757, I was sent by the Assembly to England as their agent, and by subsequent appointments continued there till 1775, when on my return, I was immediately engaged in the affairs of Congress and sent to France in 1776, where I remained nine years, not returning till 1785, and the said debts, not being demanded in such a length of time, are become in a manner obsolete, yet are nevertheless justly due. These, as they are stated in my great folio ledger E, I bequeath to the contributors to the Pennsylvania Hospital, hoping that those debtors, and the descendants of such as are deceased, who now, as I find, make some difficulty of satisfying such antiquated demands as just debts, may, however, be induced to pay or give them as charity to that excellent institution. I am sensible that much must inevitably be lost, but I hope something considerable may be recovered. It is possible, too, that some of the parties charged may have existing old, unsettled accounts against me; in which case the managers of the said hospital will allow and deduct the amount, or pay the balance if they find it against me.

My debts and legacies being all satisfied and paid, the rest and residue of all my estate, real and personal, not herein expressly disposed of, I do give and bequeath to my son and daughter, Richard and Sarah Bache.

I request my friends, Henry Hill, Esquire, John Jay, Esquire, Francis Hopkinson, Esquire, and Mr. Edward Duffield, of Benfield, in Philadelphia County, to be the executors of this my last will and testament; and I hereby nominate and appoint them for that purpose.

I would have my body buried with as little expense or ceremony as may be. I revoke all former wills by me made, declaring this only to be my last.

In witness whereof, I have hereunto set my hand and seal, this seventeenth day of July, in the year of our Lord, one thousand seven hundred and eighty-eight.

B. Franklin

Signed, sealed, published, and declared by the above named Benjamin Franklin, for and as his last will and testament, in the presence of us.

Abraham Shoemaker, John Jones, George Moore.

CODICIL

I, Benjamin Franklin, in the foregoing or annexed last will and testament named, having further considered the same, do think proper to make and publish the following codicil or addition thereto.

It has long been a fixed political opinion of mine, that in a democratical state there ought to be no offices of profit, for the reasons I had given in an article of my drawing in our constitution, it was my intention when I accepted the office of President, to devote the appointed salary to some public uses. Accordingly, I had already, before I made my will in July last, given large sums of it to colleges, schools, the building of churches, etc.; and in that will I bequeathed two thousand pounds more to the State for the purpose of making the Schuylkill navigable. But understanding since that such a work, and that the project is not likely to be undertaken for many years to come, and having entertained another idea, that I hope may be more extensively useful, I do hereby revoke and annul that bequest, and direct that the certificates I have for what remains due to me of that salary be sold, towards raising the sum of two thousand pounds sterling, to be disposed of as I am now about to order.

It has been an opinion, that he who receives an estate from his ancestors is under some kind of obligation to transmit the same to their posterity. This obligation does not lie on me, who never inherited a shilling from an ancestor or relation. I shall, however, if it is not diminished by some accident before my death, leave a considerable estate among my descendants and relations. The above observation is made as merely as some apology to my family for making bequests that do not appear to have any immediate relation to their advantage.

I was born in Boston, New England, and owe my first instructions in literature to the free grammar schools established there. I have, therefore, already considered these schools in my will. But I am also under obligations to the State of Massachusetts for having, unasked, appointed me formerly their agent in England, with a handsome salary, which continued some years; and although I accidentally lost in their service, by transmitting Governor Hutchinson's letters, much more than the amount of what they gave me, I do not think that ought in the least to diminish my gratitude.

I have considered that, among artisans, good apprentices are most likely to make good citizens, and, having myself been bred to a manual art, printing, in my native town, and afterward assisted to set up my business in Philadelphia by kind loans of money from two friends there, which was the foundation of my fortune, and all the utility in life that may be ascribed to me, I wish to be useful even after my death, if possible, in forming and advancing other young men, that may be serviceable to their country in both these towns. To this end, I devote two thousand pounds sterling, of which I give one thousand thereof to the inhabitants of the town of Boston, in Massachusetts, and the other thousand to the inhabitants of the city of Philadelphia, in trust, to and for the uses, intents, and purposes hereinafter mentioned and declared.

The said sum of one thousand pounds sterling, if accepted by the inhabitants of the town of Boston, shall be managed under the direction of the selectmen, united with the ministers of the oldest Episcopalians, Congregational, and Presbyterian churches in that town, who are to let out the sum upon interest, at five per cent, per annum, to such young married artificers, under the age of twenty-five years, as have served an apprenticeship in the said town, and faithfully fulfilled the duties required in their indentures, so as to obtain a good moral character from at least two respectable citizens, who are willing to become their sureties, in a bond with the applicants, for the repayment of the moneys so lent, with interest, according to the terms hereinafter prescribed; all which bonds are to be taken for Spanish milled dollars, or the value thereof in current gold coin; and the managers shall keep a bound book or books, wherein shall be entered the names of those who shall apply for and receive the benefits of this institution, and of their sureties, together with the sums lent, the dates, and other necessary and proper records respecting the business and concerns of this institution. And as these loans are intended to assist young married artificers in setting up their business, they are to be proportioned by the discretion of the managers, so as not to exceed sixty pounds sterling to one person, nor to be less than fifteen pounds; and if the number of appliers so entitled should be so large as that the sum will not suffice to afford to each as much as might otherwise not be improper, the proportion to each shall be diminished so as to afford to everyone some assistance. These aids may, therefore, be small at first, but, as the capital increases by the accumulated interest, they will be ampler. And in order to serve as many as possible in their turn, as well as to make the repayment of the principal borrowed easier, each borrower shall be obliged to pay, with the yearly interest, one-tenth part of the principal and interest, so paid in, shall be again let out to fresh borrowers.

And, as it is presumed that there will always be found in Boston virtuous and benevolent citizens, willing to bestow a part of their time in doing good to the rising generation, by superintending and managing this institution gratis, it is hoped that no part of the money will at any time be dead, or be diverted to other purposes, but be continually augmenting by the interest; in which case there may, in time, be more than the occasions in Boston shall require, and then some may be spared to the neighboring or other towns in the said State of Massachusetts, who may desire to have it; such towns engaging to pay punctually the interest and the portions of the principal, annually, to the inhabitants of the town of Boston.

If this plan is executed, and succeeds as projected without interruption for one hundred years, the sum will then be one hundred and thirty-one thousand pounds; of which I would have the managers of the donation to the town of Boston then layout, at their discretion, one hundred thousand pounds in public works, which may be judged of most general utility to the inhabitants, such as fortifications, bridges, aqueducts, public buildings, baths, pavements, or whatever may make living in the town more convenient to its people, and render it more agreeable to strangers resorting thither for health or a temporary residence. The remaining thirty-one thousand pounds I would have continued to be let out on interest, in the manner above directed, for another hundred years, as I hope it will have been found that the institution has had a good effect on the conduct of youth, and been of service to many worthy characters and useful citizens. At the end of this second term, if no unfortunate accident has prevented the operation, the sum will be four million and sixty-one thousand pounds sterling, of which I leave one million sixty-one thousand pounds to the disposition of the inhabitants of the town of Boston, and three million to the disposition of the government of the state, not presuming to carry my views farther.

All the directions herein given, respecting the disposition and management of the donation to the inhabitants of Boston, I would have observed respecting that to the inhabitants of Philadelphia, only, as Philadelphia is incorporated, I request the corporation of that city to undertake the management agreeably to the said directions; and I do hereby vest them with full and ample powers for that purpose. And, having considered that the covering a ground plot with buildings and pavements, which carry off most of the rain and prevent its soaking into the Earth and renewing and purifying the Springs, whence the water of wells must gradually grow worse, and in time be unfit for use, as I find has happened in all old cities, I recommend that at the end of the first hundred years, if not done before, the corporation of the city Employ a part of the hundred thousand pounds in bringing, by pipes, the water of Wissahickon Creek into the town, so as to supply the inhabitants, which I apprehend may be done without great difficulty, the level of the creek is much above that of the city, and may be made higher by a dam. I also recommend making the Schuylkill completely navigable. At the end of the second hundred years, I would have the disposition of the four million and sixty-one thousand pounds divided between the inhabitants of the city of Philadelphia and the government of Pennsylvania, in the same manner as herein directed with respect to that of the inhabitants of Boston and the government of Massachusetts.

It is my desire that this institution should take place and begin to operate within one year after my decease, for which purpose due notice should be publicly given previous to the expiration of that year, that those for whose benefit this establishment is intended may make their respective applications. And I hereby direct my executors, the survivors or survivor of them, within six months after my decease, to pay over the sum of two thousand pounds sterling to such persons as shall be duly appointed by the Selectmen of Boston and the corporation of Philadelphia, to receive and take charge of their respective sums, of one thousand pounds each, for the purposes aforesaid.

Considering the accidents to which all human affairs and projects are subject in such a length of time, I have, perhaps, too much flattered myself with a vain fancy that these dispositions, if carried into execution, will be continued without interruption and have the effects proposed. I hope, however, that is the inhabitants of the two cities should not think fit to undertake the execution, they will, at least, accept the offer of these donations as a mark of my good will, a token of my gratitude, and a testimony of my earnest desire to be useful to them after my departure.

I wish, indeed, that they may both undertake to endeavor the execution of the project, because I think that, though unforeseen difficulties may arise, expedients will be found to remove them, and the scheme be found practicable. If one of them accepts the money, with the conditions, and the other refuses, my will then is, that both Sums be given to the inhabitants of the city accepting the whole, to be applied to the same purposes, and under the same regulations directed for the separate parts; and, if both refuse, the money, of course, remains in the mass of my Estate, and is to be disposed of therewith according to my will made the Seventeenth day of July, 1788.

I wish to be buried by the side of my wife, if it may be, and that a marble stone, to be made by Chambers, six feet long, four feet wide, plain, with only a small molding around the upper edge, and this inscription:

Benjamin And Deborah Franklin 178-

to be placed over us both. My fine crab-tree walking stick, with a gold head, curiously wrought in the form of the cap of liberty, I give to my friend, and the friend of mankind, General Washington. If it were a Sceptre, he has merited it and would become it. It was a present to me from that excellent woman, Madame de Forbach, the Dowager Duchess of Deux-Ponts, connected with some verses which should go with it. I give my gold watch to my son-in-law Richard Bache, and also the gold watch chain of the Thirteen United States, which I have not yet worn. My timepiece, that stands in my library, I give to my grandson, William Temple Franklin. I give him also my Chinese gong. To my dear old friend, Mrs. Mary Hewson, I give one of my silver tankards marked for her use during her life, and after her decease, I give it to her daughter Eliza. I give to her son, William Hewson, who is my godson, my new quarto Bible, and also the botanic description of the plants in the Emperor's garden at Vienna, in folio, with colored cuts.

And to her son, Thomas Hewson, I give a set of "Spectators, Tattlers, and Guardians" handsomely bound.

There is an error in my will, where the bond of William Temple Franklin is mentioned as being four thousand pounds sterling, whereas it is but for three thousand five hundred pounds.

I give to my executors, to be divided equally among those that act, the sum of sixty pounds sterling, as some compensation for their trouble in the execution of my will; and I request my friend, Mr. Duffield, to accept moreover my French waywiser, a piece of clockwork in Brass, to be fixed to the wheel of any carriage; and that my friend, Mr. Hill, may also accept my silver cream pot, formerly given to me by the good Doctor Fothergill, with the motto, Keep bright the Chain. My reflecting telescope, made by Short, which was formerly Mr. Canton's, I give to my friend, Mr. David Rittenhouse, for the use of his observatory.

My picture, drawn by Martin, in 1767, I give to the Supreme Executive Council of Pennsylvania, if they shall be pleased to do me the honor of accepting it and placing it in their chamber. Since my will was made I have bought some more city lots, near the center part of the estate of Joseph Dean. I would have them go with the other lots, disposed of in my will, and I do give the same to my Son-in-law, Richard Bache, to his heirs and assigns forever.

In addition to the annuity left to my sister in my will, of fifty pounds sterling during her life, I now add thereto ten pounds sterling more, in order to make the Sum sixty pounds. I give twenty guineas to my good friend and physician, Dr. John Jones.

With regard to the separate bequests made to my daughter Sarah in my will, my intention is, that the same shall be for her sole and separate use, notwithstanding her coverture, or whether she be covert or sole; and I do give my executors so much right and power therein as may be necessary to render my intention effectual in that respect only. This provision for my daughter is not made out of any disrespect I have for her husband.

And lastly, it is my desire that this, my present codicil, be annexed to, and considered as part of, my last will and testament to all intents and purposes.

In witness whereof, I have hereunto set my hand and Seal this twenty-third day of June, Anno Domini one thousand Seven hundred and eighty-nine.

B. Franklin.

Signed, sealed, published, and declared by the above named Benjamin Franklin to be a codicil to his last will and testament, in the presence of us.

Francis Bailey, Thomas Lang, Abraham Shoemaker.

Originally the "lower counties" of Pennsylvania, and thus one of three Quaker colonies founded by William Penn, Delaware has developed its own set of traditions and history.

Originally the "lower counties" of Pennsylvania, and thus one of three Quaker colonies founded by William Penn, Delaware has developed its own set of traditions and history. Start in Philadelphia, take two days to tour around Delaware Bay. Down the New Jersey side to Cape May, ferry over to Lewes, tour up to Dover and New Castle, visit Winterthur, Longwood Gardens, Brandywine Battlefield and art museum, then back to Philadelphia. Try it!

Start in Philadelphia, take two days to tour around Delaware Bay. Down the New Jersey side to Cape May, ferry over to Lewes, tour up to Dover and New Castle, visit Winterthur, Longwood Gardens, Brandywine Battlefield and art museum, then back to Philadelphia. Try it! Millions of eye patients have been asked to read the passage from Franklin's autobiography, "I walked up Market Street, etc." which is commonly printed on eye-test cards. Here's your chance to do it.

Millions of eye patients have been asked to read the passage from Franklin's autobiography, "I walked up Market Street, etc." which is commonly printed on eye-test cards. Here's your chance to do it. In 1751, the Pennsylvania Hospital at 8th and Spruce was 'way out in the country. Now it is in the center of a city, but the area still remains dominated by medical institutions.

In 1751, the Pennsylvania Hospital at 8th and Spruce was 'way out in the country. Now it is in the center of a city, but the area still remains dominated by medical institutions. Grievances provoking the American Revolutionary War left many Philadelphians unprovoked. Loyalists often fled to Canada, especially Kingston, Ontario. Decades later the flow of dissidents reversed, Canadian anti-royalists taking refuge south of the border.

Grievances provoking the American Revolutionary War left many Philadelphians unprovoked. Loyalists often fled to Canada, especially Kingston, Ontario. Decades later the flow of dissidents reversed, Canadian anti-royalists taking refuge south of the border.

{kind=link}