Related Topics

Insurance in Philadelphia

Early Philadelphia took a lead in insurance innovation. Some ideas, like life insurance, flourished. Others have faded.

Dislocations: Financial and Fundamental

The crash of 2007 was more than a bank panic. Thirty years of excessive borrowing had reached a point where something was certain to topple it. Alan Greenspan deplored "irrational exuberance" in 1996, but only in 2007 did everybody try to get out the door at the same time. The crash announced the switch to deleveraging, it did not cause it.

Whither, Federal Reserve? (2)After Our Crash

Whither, Federal Reserve? (2)

Right Angle Club 2011

As long as there is anything to say about Philadelphia, the Right Angle Club will search it out, and say it.

Black Swans (Financial Variety)

|

| Nicolas Baudin |

The mouth of the Delaware River once teemed with white swans, but black swans were unknown until the French explorer Nicolas Baudin brought home a few from Australia, where they are now celebrated as the state animal of Western Australia. Empress Josephine Bonaparte was delighted with them, made them known as her birds, and thus made the term "Black Swan" more or less synonymous with rare chance occurrences. The implied inference that every white swan contains a remote potential for breeding a black one is doubtful biology, however. More likely, black swans are a distinct species -- Cygnus atratus-- confined to Australia and New Zealand, and just about extinct in New Zealand. In that view of things, the rarity of black swans is equivalent to the prevalence of black ones, mixed within the population of generally white ones. Nevertheless, for this article, it is convenient to continue the unlikely conjecture that most, or perhaps every, white swan contain a small potential to hatch a black one.

|

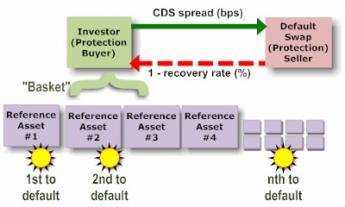

| Credit Default Swaps |

Many theories exist for the discovery that financial crises are commoner than chance alone would seem to predict; if they follow a Gaussian normal distribution curve, it must be somehow different from the distribution curve of smaller fluctuations. Observing this discordance is more or less how the phenomenon was discovered. The normal volatility of economic activity is calculated from the fluctuations observed in, say, twenty years. When that derived curve is extrapolated to include cataclysmic events which by a theory of the unmeasured "long tail" occur every hundred years, speculators have later discovered by actual measurement that, alas, such disasters actually occur much more frequently. Calculated risks derived from such extrapolations have upended many insurance companies and insurance-like vehicles like Credit Default Swaps, who set their premium charges to match the mathematics. Since CDS approached a hundred trillion dollars in the last crisis, it is important to understand the mechanics of this kind of Black Swan if we possibly can.

|

| Black Swan |

One way to do that is to question the conventional equivalence of risk and volatility ; that is, that the more markets bounce around, the riskier they become. Why should that be true, we might ask. And if it is somewhat true, why does that make it is converse true, those calm seas are safe ones? Those of us who sit and watch the ocean shore soon adopt the habit of speech that high waves at the shore mean a storm is approaching, not that it will ever arrive. After all, the center of the storm may be traveling parallel to the coastline, not directly toward it. And calm seas are particularly undependable predictors; no matter how calm it may be, the next storm might arrive in a few hours, or it may not come for months. Many other analogies spring up, once one puts aside the basic assumption that world economies can be depicted as a linear electrocardiogram. At the very least, they are two-dimensional, possibly three. Possibly four, if you regard time as a dimension.

|

| Dow Jones |

It must be noticed that market volatility is universally viewed as linked to bad things, and many efforts have been made by central banks to reduce risk by constraining volatility. Alan Greenspan is famous for having controlled the economy for seventeen years without major depression. Is that necessarily a good thing? Is it equally possible that kinetic energy was constrained within the inflating balloon until the bursting of it was a far more damaging explosion than small planned deflations would have been?

Experimental testing of these ideas has itself been constrained by an inability to predict the explosion point of expanding financial balloons. Planned deflations have been particularly feared, because of lack of assured ways to get them to stop deflating. But practical warnings such as these are not the same as claiming that lack of volatility is always the ideal state.

Originally published: Thursday, May 26, 2011; most-recently modified: Sunday, July 21, 2019