3 Volumes

Second Edition, Greater Savings.

The book, Health Savings Account: Planning for Prosperity is here revised, making N-HSA a completed intermediate step. Whether to go faster to Retired Life is left undecided until it becomes clearer what reception earlier steps receive. There is a difficult transition ahead of any of these proposals. On the other hand, transition must be accomplished, so Congress may prefer more speculation about destination.

Handbook for Health Savings Accounts

New volume 2015-07-07 23:31:01 description

Consolidated Health Reform Volume

To unjumble topics

(2) Obamacare: Spare Parts for a Book

New topic 2015-07-22 16:02:02 description

Pit Stop #2: What Are the Foreseeable Consequences?

We have now traversed the outline of the Health Savings Account proposal to finance the growing burden of its cost. It can be viewed as a transfer mechanism to shift a great deal of money from the savings of the population, into the common stock of its major businesses, generating a great deal of wealth in the process intended to pay for payment shortfalls which would otherwise disrupt the economy. Eventually, this growing shortfall would otherwise become so large it would curtail the medical progress we wish to expand. The direct losers in this disruption would be the financial industry, and probably the insurance industry, but the ripples would spread far and wide. The following discussions center on features familiar to the author, more than they do on issues better known to others. In time, experts in related fields are invited to participate, because predicting the future is always fraught with uncertainty.

The groups to be discussed as primarily affected are:

The Recipients of Care: CHAPTER SIX

The Providers of Care: CHAPTER SEVEN

The Financial Services Industry: CHAPTER EIGHT

International Finance : CHAPTER NINE

Retirees: CHAPTER TEN

The Education Industry: CHAPTER ELEVEN

Recipients of Care: CHAPTER SIX

Under the HSA plan, subscribers between age 26 and 65 are in the age group most likely to be employed, and so the original act provides a maximum annual contribution of $3300. A maximum was probably thought necessary to prevent gaming and arbitrage between taxable and non-taxable income, and it has proved ample for most HSAs of the regular, annual, kind. Now that enrollments have been frozen at the age of 30, this limit probably is adequate for the moment, although it generates a need for catch-up contributions to equal the amount that more affluent subscribers were able to contribute. Looking forward to a hoped-for relaxation of the age 30 limit, another catch-up will probably be necessary, possibly included under a provision allowing cumulative amounts to be deposited, to replace year-by-year limits. Otherwise, the $3300 limit is probably not burdensome, since it would stretch the abilities of young subscribers to meet other expenses characteristic of their age group. It's quite a bargain, however, potentially offering $325,000 worth of healthcare for $132,000.

Whether or not this offer is greeted with gratitude or with jeers, it will surely stretch the budgets of many young families. Perhaps the age group should be segregated into two or three groups to meet the resources more realistically, but the invincible facts of compound interest are that the younger you are when you contribute, the cheaper the package becomes.

Looking beyond the paycheck, this $132,000 includes the likelihood that the Medicare payroll deduction might be forgiven. It is hard to know how this age bracket would respond to the offer of buying out Medicare for $80,000, or even $40,000 if the decision is made to pay off the existing Medicare debts in some other way. For some people, $40,000 is the price of a mid-sized car, but for others, it would seem an insurmountable goal. However, attitudes may well change. As this generation approaches age 65, the difficulties of accumulating enough money for a thirty-year retirement will surely be more apparent, and $40,000 will seem less formidable.

The other side of it will appear when interest rates return to normal. At the moment, $40,000 in index funds compares very favorably with the 1 or 2% available in a savings account. Much will also depend on whether the tax exemption for employer-paid health insurance is continued. At present, health insurance provided by an employer appears to be free. That appearance will fade as the pay packet adjusts upward to compensate, but the employee will probably have to fight for it, and harbor some resentment that something has been taken away.

Removing the tax advantage. At the moment, I have two suggestions for making this transition easier. The first would be to extend the tax preference to self-employed and unemployed persons. Following that, lower the tax preference for everyone by at least 25%. That would be approximately revenue-neutral.

The other suggestion is bolder but more advantageous. That is, to leave the Henry Kaiser tax exemption on the books, but lower the corporate income tax. It's double-taxation, to begin with, and the employer would enjoy no tax benefit if he became tax-free. Unfortunately, the experience of Ireland was that lowering the tax too abruptly caused foreign companies to move in Ireland, and the disruption to Ireland was extreme. The Irish experience is a vivid example of the need for monitoring these changes closely and making quick mid-course adjustments. International agreements with trading partners would also be helpful. It must be remembered that corporate donation of health insurance is a major financial support to healthcare, the tax abatement representing almost half of corporate revenue, and almost an equal amount from the employee taxes. It is something of a puzzle to know whether the double taxation of corporations does or does not double the support of business to healthcare costs. The other side of it is the apparent free lunch comes close to doubling the cost of healthcare through using the insurance mechanism to make it appear free. It is very hard to escape the suspicion that this tax preference puzzle can explain most of our cost escalation, compared with other developed nations.

Providers of Care: CHAPTER SEVEN

Since it's pretty clear the widespread use of health insurance has led to increased healthcare prices, it follows that curtailing insurance will lead to lower prices. Let's repeat that: Health Savings Accounts will lower healthcare prices. In the case of physician fees, downward pressure on prices might be somewhat lessened by whatever price resistance had been successful since the administration of Lyndon Johnson. But at least the medical profession has a long and formal history as a fiduciary, and both the voluntary hospitals and the retail pharmacists have a similar tradition of placing the interests of the patient ahead of their own. Local corner drugstores have essentially disappeared since the chain stores put in an appearance, however, and it's a bad omen for any others with some history of fiduciary behavior. On the other hand, more recent entrants to the third-party world, like nursing homes, therapists, and vendors of medical supplies, have a little tradition of charitable behavior. They can expect a purely commercial response to reduction of insurance, which the more benevolent professions will feel is justified, even to the extent of seeing the others disappear, just as the other professions resisted their inclusion in insurance, in the first place. Most of this infighting will take place far below the surface of the water, and the public may be spared much insight into why the acupuncturist survives or even prospers, while the occupational therapist may not.

The hospitals and doctors will probably have an interesting time together. We have earlier described how DRG suppressed hospital inpatient prices, leading hospitals to emphasize emergency room and outpatient services with some pretty fancy pricing. What's more, to fill up these outpatient areas, an epidemic of purchasing physician practices has been encouraged, not merely by the hospitals, but by the administrative rules of the insurance companies. This trend has been most pronounced in rural areas, and rural areas will probably lead the response when the rules change. A rather alarming town-gown schism has made its appearance, with group practices and university hospitals directly attacking the ability of office physicians to select the hospital or group practice which suits them best. When more control of referrals inevitably reverts to unsalaried and unaffiliated physicians, some of the retaliation may be rather unseemly.

In the long run, it is the patients who will decide the bulk of these little quarrels, and the ultimate loyalty of the patients has not been specially cultivated by the teaching hospitals. In England, the loyalty of patients to the Health Service has been surprising even to the politicians, whereas the physicians have been less than thrilled. In Canada, however, the loyalty of physicians to the system of fee-less practice has been at least as strong as their irritation at its regimentations. That is, the position of Canada is strangely reminiscent of its position in the Revolutionary War, midway between the Mother Country and its rebellious colonies. Whether or not this reflects the same sociological causes, must be left to historians to reflect upon. To the South of us, the same persistence of cultures can be found, but with the prosperous classes demonstrating their understanding of the power of money, and the poor classes affiliating with the position of giveaways in class warfare. In all of these local examples, there is a strange tendency for personal self-interest to have less influence than economists typically would suppose.

It is hard for most people to remember the dilapidated, run-down conditions of American hospitals in 1945. This is usually blamed on the Great Depression or the two great World Wars. But a glance at public buildings of the various eras, or public transportation in the same economic cycles, brings up a different possibility. Perhaps the neglect of the public sector is the default position of democratic societies, only breaking free of it, during periodic episodes of prosperity. Or, conversely, perhaps the default position in everybody's mind, is the condition he noticed in his own childhood.

Retirees: CHAPTER NINE

Retirees are the main readers of newspapers and periodicals, so it is not surprising to find the media full of stories about the retired elderly. What seems underestimated in all this discussion, is the plain fact that civilization has never experienced such an expansion of more or less healthy longevity, ever or anywhere. We dare not rely on tradition or our own experience, because there is none. Whatever will old folks do without Medicare? Or, when the money runs out, without Social Security, defined benefits pensions, nursing homes or retirement villages (CCRC). Are ya gonna need me, are ya gonna feed me, when I'm a hundred twenty?

The point to quoting the Beatles song of the sixties is their punch line of "sixty-five" has become "hundred-twenty" in less than a generation. For a while, President Bush thought the depletion of Social Security would be the first snowflake in a blizzard, but now we have forgotten that particular misjudgment, and find that paying for Medicare is going to seem a problem, first. The problem is not one or the other, the problem is longevity. The impossible dream has become very possible, and we don't know what to do with it.

It seems to me, one thing is very clear: we cannot expect to work for forty years but live an additional fifty years being supported. It is childish to suppose someone else (the millionaires and billionaires, our parents and grandparents, or the taxpayers) will support us for 20% longer than we support others, or that on average we can do it for ourselves. Earning interest on savings will help the present problem, and I have here contributed some suggestions about it. But in the long run, the long run will win. So if there is any solution possible for this longevity problem, it must lie in most people remaining gainfully employed, at least ten years longer than we now think is reasonable.

Any further extensions of longevity will have to be paid for by working still longer. In the meantime, we must save and invest more wisely, at whatever cost to the retail financial industry. I have scarcely ever met a stockbroker I didn't like, and it pains me to ask the retail brokers to do what the medical profession is committed to doing: do our job so well, we put ourselves out of business. The financiers stand astride the information pool, from which a solution to this problem would be expected to arise, and they resist the idea they are fiduciaries. That's got to stop, not because an occasional account is being churned, but because they are the logical people to devise a solution to society's current big problem. Ordinarily, you wouldn't expect doctors to solve a financial problem, you would expect financiers to do it. Maybe college professors of economics would stop crabbing so much, and help with the theoretical problems of finance, but generally speaking one would expect the solution to financial problems to arise from the financial community. Where are the customers' yachts?

The problems financiers need to help us with are not so much the sharing of profits generated by efficiency, either. Looking further ahead, it worries me to have so large a proportion of common voting stock in the hands of people who, although the owners are all right, are not in the least interested in voting their stock. As the proportion of voting stock shrinks in the hands of those who know something about the company they own, the welfare of the company is not necessarily improved. The way family-controlled corporations outperform public-controlled ones by 15-25% is maybe a signal we are making things worse. And furthermore, if essentially unlimited amounts of money pour into the stock market, the value of money is lessened, the value of a stock is temporarily increased, and we suddenly wake up to realize by going off the gold standard we have not replaced it with anything else. The resulting temptation to print bitcoins or paper without value seems ominous. What is proposed we do about it, if Argentina or similar public servants somewhere else, start printing money? I am not comfortable letting Mr. Putin decide such questions, but if he tries it, what are our plans?

The Streets of Philadelphia, on Ben Franklin's Birthday

|

| Benjamin Franklin 309th Birthday |

They changed the calendar in the Eighteenth Century, so it's always confusing to talk about the birthdays of the Founding Fathers. Benjamin Franklin for example was born on January 6, 1705, but by the time he got around to being famous, he was born on January 17, 1706. Scholars handle this awkwardness by saying he was born on January 17, 1706 [OS, January 6, 1705]. That's not all the problem, however. This year on January 17 he had his 309th birthday, unless you wish to say he had his 310th birthday on January 6. The novelty has long since worn off, and nowadays most birthday celebrants prefer just not to mention the matter. You might think Don Smith would think this is of vital importance, but he cheerfully brushes it off with a chuckle.

|

| BenFranklin Celeabration |

Don Smith is the current leader of the Ben Franklin Birthday Celebration, which is held at 9 AM every year, on January 17th [NS], starting at the American Philosophical Society's Franklin Hall on Chestnut Street, once a very substantially-built bank building. The constituent members are affiliated with one of the thirty-odd organizations which Franklin founded, although anyone interested is welcomed. On what usually turns out to be the coldest day of the year, the birthday celebrants gather for hot drinks and cookies, followed by one or two really outstanding lectures about Franklin. Sometimes the lecture's connection to Franklin is a little stretched, but all of them are excellent. At 11 AM, the group marches together to Ben's grave at 5th and Arch for a short ceremony, led by Franklin re-enactors and honest-to-goodness members in the uniform of the National Guard, which Franklin founded. He did so when the Spanish and French ships were bombarding the coast, and as the editor of the town's newspaper, Franklin called for troops to defend us. The Quaker government declined to be violent, so Franklin published an invitation for volunteers to bring their guns and join him. Ten thousand showed up, and Franklin's career in public life was established. He was a hero to everyone -- except Thomas Penn, who saw him as a threat. Much subsequent Colonial history revolves around this episode and its consequences.

After the march, the group settles down for a good lunch, and hears yet another outstanding lecture. This year it was given by Paul R. Levy, the President of a planning organization called the Center City District. Steve's message this year was about how the streets of Center City Philadelphia were constructed for walking, or at most riding horseback. That is, they were narrow. They widened somewhat as they went West and had to accommodate a city of carriages. That was quite good enough through the Gilded Age, when Philadelphia could credibly claim to be the richest city in the world.

|

| Auotmoblie |

But then what happened was not the two World Wars, the stock market crash of 1929, or anything resembling that. What happened in Paul Levy's view, was the automobile. Hundreds, then thousands of autos filled the streets, scattering chickens and children, and eventually making the city impassible. Nothing would do but to move to the suburbs, which among other things provided the thrill of driving too fast and too carelessly, and reducing the pedestrians while increasing the business of accident rooms. There was certainly no room for bicycles, which were driven away without a tear being shed, and defying the efforts of city planners to find a safe place for them. Europe, good old Europe where we came from, was more successful in hounding the imposter autos off the bike paths of Amsterdam and Copenhaven. And preserving intercity high speed train service, at great taxpayer expense. Those Europeans really know how to live, in sidewalk cafes, unaffected by bicycles, preserving a much older collection of narrow city streets leading to empty cathedrals, in Germany, France, and Central Europe. That wasn't the American way, at all. We just pulled up sticks and moved to the suburbs, abandoning the dirty old defeated cities to their ethnic neighborhoods.

It's a novel theory, and maybe even a correct one. It could explain a lot, if Philadelphia is seen as a victim of Detroit, strangling on their mutual industrial excesses.

The Math of Predicting the Future

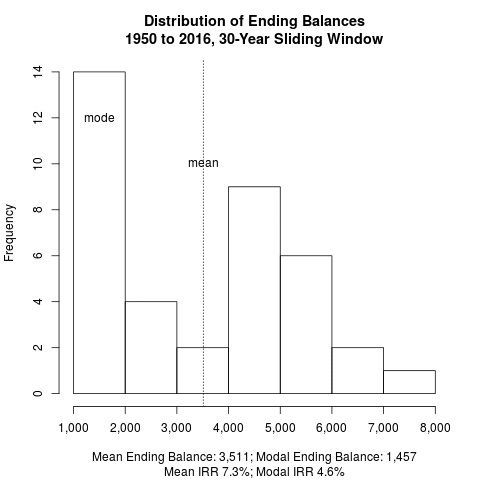

The accuracy of predicting future longevity, future health costs, and future stock markets -- is individually very low, so aggregated numbers can be (at least) equally misleading. However, they are the best available guides to the future. The purpose of deriving them (Mostly from CCS data) is to surmise whether it is safe to proceed with a trial of concepts. While the differences are great their direction is nevertheless pretty clear: Substituting the HSA would surely save a great deal of money, compared with Obamacare or Medicare. Why not substitute it for both Obamacare and Medicare? Transition costs are not estimated, and no doubt would be considerable, even if one plan replaced several others. Overall HSA cost is inversely related to investment income; three levels of income are presented, but a conservative conclusion is argued.

In short: HSA could just about replace both ASA plus Medicare, with a long transition period. But one must be more hesitant to suggest they can stretch to reducing accumulated Medicare debts from past spending. My guess is preventing more international debts is all we can promise. Someone else must figure out how to pay the existing debts. Why include Medicare, then, if predictions are sketchy? Two main reasons: my opinion is that funding Medicare is a worse problem than insuring younger people; it is not fixed, nothing else can be successfully fixed.

Second, it is such a political third rail of politics to talk of revising Medicare that someone with nothing personal to lose, like myself, must start the discussion. Some other funding source must probably be found to eliminate the existing Medicare debt, but there's not much risk of needing the money very soon. I am also a little apprehensive about the decline of existing Treasury bonds when interest rates rise because so many of them have been issued to cope with the recession. Any appreciable reduction of Medicare costs could accelerate a rise in bond interest rates, which would send the market price of existing bonds downward. Therefore, even a move in the right direction must include a reverse button, and be coordinated with the Federal Reserve. It is most unfortunate that Medicare is both more serious and more manageable, while at the same time it is so politically dangerous.

Paying to Replace Medicare and Debts with Health Savings Accounts. At least, savings to the consumer for the combined ASA and Medicare replacement would be returned to the subscriber as payroll-deductions and premiums-eliminated, (i.e., About half of the Medicare cost.) Savings from replacing Obamacare would be even greater, but from my viewpoint, such savings would all be poured into rescuing Medicare. That's ironic because it is the reverse of what the elderly are fearing. Even Obamacare advocates should welcome the elimination of Medicare because its losses are dragging everything else down. Unfortunately, this is not well understood by the public, who love Medicare. (Everybody loves to get a dollar for fifty cents.) Somebody has to say this can't last, and I guess I'm it.

To be confident Medicare's costs plus its debts would actually be manageable, the average subscriber would have to contribute about $1600 a year for 40 years to an escrow fund at 6% annual income. That's to achieve a total of $246,000 on his 65th birthday, paying his ordinary health debts from 25 to 65 with the other $1700 of his allowed Health Savings Account deposits, to pay average medical expenses for age 25-65. In my opinion, it can't be done.

You might subsidize poor people in the name of fairness, but this is how much you have to find, somewhere, to pay present costs. You might try raising the annual limits for deposits into Health Savings Accounts, but this would prove futile if too few people could afford to pay it. If you please, health expenses would then have to be cut enough to pay for the subsidies, unless the subsidies are cut to pay the health expenses. With that and a continuation of 6% return as long as the paying subscribers live and the fund remains solvent, we might make it. It is my hope that using private markets rather than Treasury rates, pay down of the debt can be accomplished with higher interest rates, but it is uncertain even this can be done. High rates like that are only likely to appear if inflation starts to gallop, or some other cataclysm intervenes, with the following result: the virtual value of the Medicare debt erodes, and the creditors lose much of their loan in real value. Some individuals might be able to manage their cost, but it's very hard to believe it could be an average performance for the whole nation. This is not an easy problem, and it becomes impossible if disillusioned Democrats block it.

And yet, the nation has already made it official it is going to spend nearly twice that amount, while only getting Obamacare in return. If the President is right about his side of it, then getting Medicare free in addition, is do-able by this Lifetime Health Savings Account alternative. If not, then both have to be scaled back. Big business is about the only hope, using a cut in corporate taxes as bait. This would be a big step since if they don't pay corporate taxes, they don't need a tax exemption for healthcare; they already have cut their tax bill.

Present law permits $3300 annual HSA deposits to age 65, or $132,000. With only 6% compounded interest income included to reduce the cost, Health Savings Accounts could only have a net lifetime out-of-pocket cost of $58,000, no matter what healthcare expenses are actually incurred. By my estimation, this is only half of enough. Sometime in the future, inflation will force this limit to be raised, and it should be linked to some external inflation measure like the Cost of Living Index, although a healthcare cost of living index would be closer to what is needed. Inclusion of tax exemption for the premium of catastrophic high-deductible policy which is required by law, would not only be more equitable but perhaps could provide both a superior COLA and an external measure of average Catastrophic premiums for marketplace judgments. It is probably undesirable to create an arbitrage opportunity between taxable and after-tax choices with infrequent, steep-step, changes in the deposit limits, so these limits should somehow be adjusted annually. Annual limits should be supplanted with lifetime limits whenever the account is depleted below a certain fraction of the buy-out price, which should be maintained and upgraded for this purpose. Since expenditures are limited to healthcare, a liberalization of this catch-up limit is urged.

There is thus room to spare, here, as well as for increasing 6% return in the direction toward 10%. Since the investment scene is in flux, more experience may be necessary for better guidelines. Depending on the interest rate actually achieved, and the choice between maximum allowable, or less out-of-pocket, lifetime Health Savings Accounts could cost somewhere between 58 and 132 thousand dollars, lifetime total average, in the year 2014 dollars. The Medicare escrow part of that would be $10,000, and Catastrophic coverage for 58 years of Medicare life expectancy would add $58,000. The deposit costs for the Obamacare years 25-65 would themselves total $10,000, and estimated Catastrophic insurance would add $16,000, to a total lifetime cost of $26,000. If contributions are raised, there's room for it under the $3300 yearly limit. The hard question is whether we could get $3300 on average for forty years, and I'm not sure we can. Please note: HSA deposit costs should remain linked to the 40 working years 25-65, but investment income would be realized over the entire 58 years. For the purpose of extending interest income, HSA coverage could be extended another 40 years, but this would mostly be an illusion. Real wealth is only generated during the working years. Depositing extra money in an HSA is not entirely a bad thing, because if you deposit more than you need for medical care, you will get the excess back, multiplied by tax-free investing. However, if people can't afford to do it, they won't. Obviously, the same cannot be said of buying too much insurance, where the insurance company profits from those who drop their policies..

Compared With the Affordable Care Act. Now, compare: the cheapest bronze Obamacare cost (covering 60% of healthcare, age 26 to 65) is $288,000, accumulated and paid for over a 40-year span. Adding Medicare adds $95,400, made up of $23,800 of payroll deductions, $23,800 of premium collections, and $47,700 of debt, accumulated over 18 years, paid for over 40 working years. Obamacare followed by Medicare is what we are officially destined to get. Total average lifetime costs are thus projected to be $383,300, plus the 40% estimate of uncovered ACA costs under the Bronze plan. Considering different inflation assumptions and rounding errors, that's pretty close to the $325, 000 which was calculated by Michigan Blue Cross and confirmed by federal agencies, for year 2000. To repeat, this is what we will get unless it is changed. Restating the calculations in words, healthcare is, therefore, being treated as if it were entirely self-funded, generating no losses but also generating no income on the sequestered premiums. The hidden restatement would be: the present and projected healthcare system is running at a loss, it generates no net income on what ought to be very large reserves, and nothing is being done to make it break even, to say nothing of generating income.

This outcome makes me absolutely confident we can do better. The lifetime Health Savings Account would create immense savings, which by rough calculations would be somewhat less confidently stated to be savings of $190,000, in year 2014 dollars, per lifetime. Multiply that number times 340 million citizens, and you get a result in the trillions of dollars. It's pretty staggering to confess that even this much improvement may not be enough.

............................................................................................................................................................................................................................................

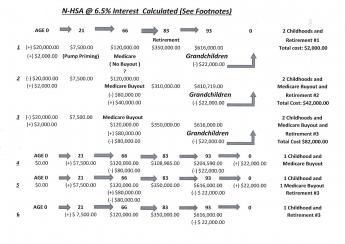

Comparisons of Health Savings Accounts Escrow for Medicare Costs (est.)

Lifetime Health Savings Account (68 yrs.)............vs................Medicare alone.

..............$80,000 single payment(40 yr. deposit of $850 =$32,000 cost, 68 yrs.@4% cmp. Interest)..*(+$18,000)

..............$160,000 single p. plus existing-debt service (40 yr. annual deposit of $1700=$68,000 cost, 68 yrs.@4% cmp. Interest)*(+$18,000)..

..............$150,000 both + subsidy (40 yr. annual deposit of $1600=$32,000 cost, 68 yrs.@4% cmp. Interest)*(+$18,000)..

..............$246,000 stretching (40 yr. deposit of $1600=$64,000 cost, 68 yrs.@6% cmp. Interest)*(+$18,000)..

..............$706,000 workplace insurance (40 yr. deposit of $3300=$132,000 cost, 68 yrs.@10% cmp. Interest)*(+$18,000)..

..............*$18,000 (Catastrophic Insurance, est. @$1000/yr for 18 extra years)

--->Total Extra Cost per Individual including Catastrophic for 18 yrs. estimate: $98,000 (18-118,000)<---

--->Present Medicare Pre-payment Costs: $196,200 plus 196,200 in debt.<---

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

Yearly Personal Expense for Forty Years, Age 25-64 (HSA vs. Obamacare) | |

|---|---|

| Health Savings Account Deposits | |

| @ 10%.....$65 per year (plus $1000 for Catastrophic coverage.) | Lifetime Cash:$2600 plus $58,000=$60,600|

| @6%......$400 per year (plus $1000 for Catastrophic coverage.) | Lifetime Cash:$1600 plus $58,000=$76,600|

| @ 2%......$2200 per year (plus $1000 for Catastrophic coverage.) | Lifetime Cash:$88,000 plus $58,000=$146,000|

| ....$3300(Maximum Legal Limit)............ | Lifetime Cash:$132,000 plus $58,000=$190,000|

| Affordable Care Act "Bronze" Premiums: $5500-$7200 (for 60% coverage of Healthcare costs)Lifetime Cash:$220,000-$288,000 |

............................................................................................................................................................................................................................................

............................................................................................................................................................................................................................................

Medicare Advance Payments, Age 25-83 Under Two Systems (HSA Escrow vs. Medicare Costs)

Health Savings Account,Escrow Deposit............||||||...................................... Medicare Yearly Program Costs......................................

@10%...............@6%...................@2% ..|||||...............Payroll tax...................Premiums......................Debt............

$45.................$250.00..................$1400...........|||||||............$1320......................$2640 (x18yrs).............$2725 (x18yrs.).............

----------------------------------------------||||||-----------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------------------

............................................................................................................................................................................................................................................

Total Cost per Individual including Catastrophic for 68 yrs. estimate: $127,500.Total Cost if health insurance were tax deductible including Catastrophic for 68 yrs. estimate: $88,800.

....................................................................................................................................................................................................................................................

Limit per Individual, Exclusively used for Medicare Pre-payment: ($3300/yr x40= $132,000, realizing $1,460,000 at age 65 @10%.)............................

-------------------------------------------------------------------------------------------------------------------------------------

Multi-year Health Savings Account (40 yrs.)............vs..............60% of Affordable Care alone.

...............$56,000 (1800-58,000)............................$288,000

....................($83/mo)...................................................

Total Cost per Individual, median estimate.

-----------------------------------------------------

Multi-year Medicare Escrow Deposits (40 yrs.)............vs..............80% of Affordable Care alone.

...............$80,000............................$288,000

Multi-year Medicare Escrow Deposits (40 yrs.)............vs..............60% of Affordable Care alone ("Bronze").

...............$80,000.($850/yr @4%, 150/yr @10%, contributing from age 25-65 ). ..........................$288,000

Estimated $18,000 Catastrophic Coverage Escrow (18 yrs.), escrow released at age 65

...............$ 8000 ($200/yr @4%, $40/yr @10%, contributing from age 25-65)

Total Medicare Escrow Cost per Individual, median estimate: $89,600 ($1050/yr @4% investment income, $190/yr @10%)

--------------------------------------------------------------------------------------------------------------------------------------

Lifetime HSA plus Medicare............vs................Affordable Care plus Medicare

.........$120,000 (1800-58,000)............................$484,000 plus 196,000 in debt.

................($166/mo}.......................................................................... Total Savings per Individual, median estimate: $190,000

---------------------------------------------------------------------------------------------------------------------------------------

All costs assuming age 25 to start depositing. Transition costs at later ages are not calculated. ---------------------------------------------------------------------------------------------------------------------------------------

Epilogue: Where Does All This Money Come From?

Although this book promised, and I hope delivered, a detailed discussion of how Health Savings Accounts might work if Congress unleashed them, the original question remains. Where does so much money come from? Well, in one sense, it comes from saving $350 per year, starting at age 25 and ending at 65, earning 8% compound interest. That's if longevity remains at 83. We assume the average person has medical expenses, but we don't know how to estimate them, so we put $350 a year in escrow, and average person has to contibute more cash for medical expenses at 80 cents on the dollar (the tax exemption) until experience shows he has five or ten years pre-paid, or until he reaches an estimated cash limit. Somewhere around that point, he can stop contributing, both to the escrow fund and to incidental medical costs, until the fund catches up with him. In plain language, he gives himself a loan if his expenses are too high. These figures are based on current average costs, so the money is calculated to be present in the fund but poorly distributed. After experience accumulates, these numbers can be readjusted from present over-estimates..

The prudent way to manage future uncertainties is to over-fund them and transfer any surplus to a retirement fund.

|

| Planning For The Future. |

The amount of contribution to the escrow fund could be reduced to actual costs over time, but the prudent way to manage uncertainties is to over-fund them, planning to roll any surplus over to a retirement account. Three-hundred-fifty million Americans, times $350,000 apiece in lifetime medical costs, results in a number so large it requires a dictionary to pronounce it correctly. Cutting it in half still suggests a financial dislocation of major proportions, so out of whose pocket would it come? Even if it's a win-win game, dumping that much money into the economy sounds destabilizing. These are not legitimate reasons to avoid it, but it seems hardly credible it could happen without someone noticing a big difference. What does it do to the monetary system?

If it is assumed funds generated by this system are ultimately used to pay off accumulated debts, the result should be some degree of deflation. The Federal Reserve has already purchased several trillion dollars worth of bad debt so debt repayment would not seem to pose a threat. By contrast, inflation could become a threat if corporate taxes are reduced too rapidly, but presumably, we have learned the lesson of lowering Irish corporate taxes too rapidly. Because of international ramifications, we have to assume this threat would be recognized. Because of the nature of compound interest, it has the least effect in its early stages, and there would be sufficient warning of inflation to mobilize action. Interest rates would probably rise, but there is a cushion of several years of subnormal rates, and most people would feel the elderly have suffered enough from low rates to justify some relief.

A certain amount of trouble resulted from using the "pay as you go" model, in which current premiums pay for current expenses. That is, the money from young healthy subscribers pays the bills of old, unhealthy, ones. By that reasoning, the original subscribers in 1965 got a free ride from Medicare and never paid for it. The debt has been carried forward among later subscribers, and although it is a debt which still remains to be paid, it seems very likely no one would ever collect it. Each generation makes it a little bigger by adding subscribers and running up hidden debt charges, but at least it is accounted for. In a way, there is enough guilt feeling about this matter, that it would probably be politically safe to create a balancing fund, to be used in case there are monetary issues with this unpaid indebtedness.

Let's remember that a major part of the health financing problem can be traced to the unequal taxation exemption of big business, which traces back more than seventy years to World War II. No one welcomes reducing net income in half by any means, but reducing corporate income taxes might just be one of the few ways it could be an inducement. No taxes, no tax exemption; it sounds pretty simple until you review the trouble the Irish Republic got into when it reduced them too fast. But when corporate taxes are the highest in the world, and international trade is threatened -- is certainly the best time to do it. And politically, when wealth redistribution has just been given a thorough pounding in the polls, is also a good time to advance the idea. If everyone would be reasonable about the details, an important tool for managing international trade could be fashioned out of needed healthcare reform. It certainly is a double opportunity.

|

A fiduciary puts his customer's interest ahead of his own.

|

| The End of The World? |

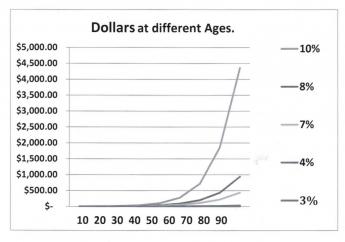

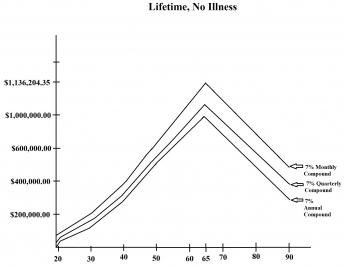

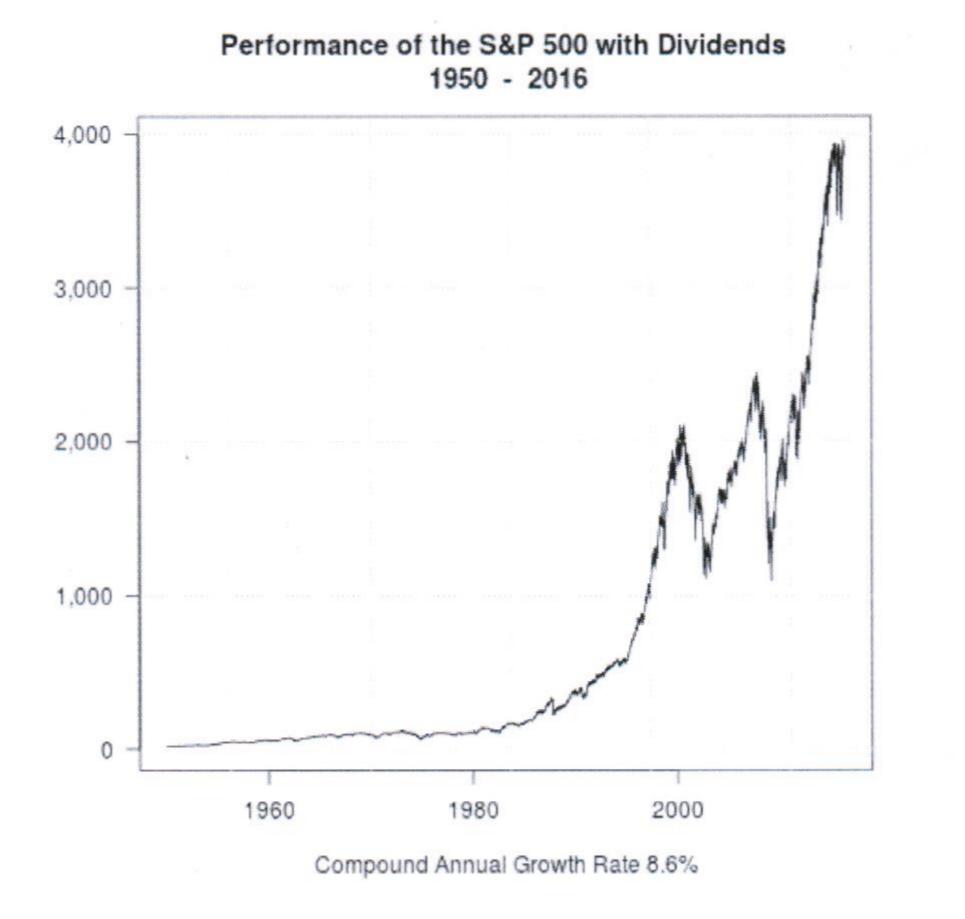

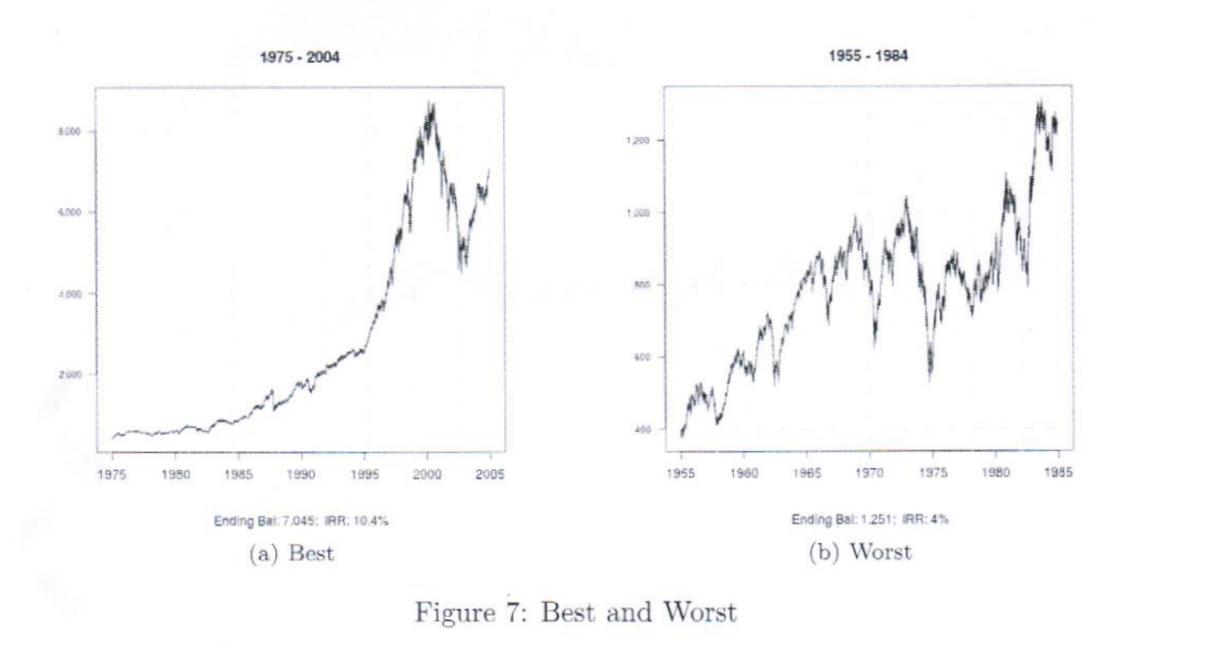

We mentioned earlier, Roger G. Ibbotson, Professor of Finance at Yale School of Management has published a book with Rex A. Sinquefield called Stocks, Bonds, Bills and Inflation. It's a book of data, displaying the return of each major investment class since 1926, the first year enough data was available. A diversified portfolio of small stocks would have returned 12.5% from 1926, about ninety years. A portfolio of large American companies would have returned 10.2% through a period including two major stock market crashes, a dozen small crashes, one or two World Wars hot and cold, and half a dozen smaller wars involving the USA. And almost even including nuclear war, except it wasn't dropped on us. The total combined American stock market experience, large, medium and small, is not displayed by Ibbotson but can be estimated as roughly yielding about 11% total return. Past experience is not a guarantee of future performance, but it's the best predictor anyone can use.

During that most recent prior century, we had a lot of crisis events, which normally bump the stock market up and down. A standard deviation is an amount it jumps around, and one standard deviation plus or minus includes by definition two-thirds of all variation. During the past ninety years, the standard deviation has been 3 percent per month or 11% per year. Standard deviations for the whole century are not meaningful because of more or less constant inflation. Throughout this book, we repeatedly describe investment income as 10%, for a simple reason: money compounded at 10% will double every seven years. Using that quick formula, it is possible to satisfy yourself what 11% can do if you hold it long enough. Since no one knows what will happen in the next 100 years, it is futile to be more precise. We may have an atomic war, or we may discover a cheap cure for cancer. But 10% is about what you can reasonably expect, doubling in seven years if you can restrain yourself from selling it during short periods when it can deviate less or more. The most uncertain time is immediately after you buy it before it has time to accumulate a "cushion". As we see, your money earns 11%, but it isn't necessarily what you will earn.

|

Your money earns 11%, but that isn't necessarily what you will earn.

|

The last few paragraphs sound like a digression, but they aren't. The question was, Where does all this money come from? Would there be wealth creation if the system favored the retail customer more, or wouldn't there be. I don't know the answer, but one likely approach is, let's try it.

Financial Overview

A More Uniform Healthcare Accounting. Here is how to pay for lifetime healthcare. Consider it's a flat tax, in the sense of everyone of the same age paying the same amount. But it's also progressive, in the sense that average amounts vary at different ages. You might say it's a flat tax, more realistically adjusted for age. At least, in theory, children borrow from parents, paying back when older. Old folks, by contrast, use up savings they themselves had accumulated while middle-aged. The existing healthcare payment system is not greatly different, except for how Medicare is sourced out.

Thus, the average child and young person, in theory, ought to borrow from, and repay, his parents. But ordinarily, there isn't enough money in his account to allow it. If there isn't enough aggregate money within the whole healthcare system, it must be supplied from tax subsidies. There are no social classes of permanently rich and poor; just people of different ages, so income tax subsidies are add-ons, considered separately. Income tax is not a flat tax, so subsidies derived from it represent richer people paying for poorer ones. To summarize: all new wealth can be traced back to people of working age. They pay for their children, and they save for themselves, for later. Their children may never pay them back, and their savings may not cover the needs of old age. Nevertheless, for practical purposes, all wealth is generated between ages 26 and 65, often in differing amounts.

The Medicare Exception. It reduces complexity to view it uniformly, and it immediately unravels Medicare as an outsider. There's a great contrast in Medicare, where we only pay for one-quarter of Medicare with payroll deductions in the normal way of saving to pre-pay a coming expense. A second quarter of the cost is paid by elderly subscribers themselves as premiums. But the real problem is generated by paying the remaining half of the cost, in appearance by taxing the working class, but actually by immediately borrowing it from foreigners. If it's ever going to be paid in the future, it adds additional hidden interest cost, so more than half really isn't in full circulation, yet. No wonder it's popular; the public thinks it's getting a dollar's worth of health care for fifty cents.

|

Tell me what you can spend, and I will predict the costs.

|

For example, if you think a 26-year-old can invest more than $3300 a year in his lifetime healthcare, go right ahead and some more revenue is available for politicians to spend. I happen to think this is at, or beyond the ability of a 26-year-old, so anything more than $3300 must come from some other age group, which will naturally resist. Anything borrowed from foreigners makes the whole thing -- non-self sustaining. You will have to elect magicians to make it come true for very long. From age 26 to 65, the system thus acquires $132,000 aggregate per person but spends $350,000. If that isn't good enough, just spend less, die younger, or rely on the black magic called outside debt. Where does the difference come from? From 8% compound investment return, passively invested in nation-wide index funds. And it won't come easily; you will have to scratch and claw for every penny of it.

Total revenue is $350,000, composed of $132,000 in direct contributions by working-age people, plus $218,000 in that compound investment income. To accomplish it, you must be dealing with agents who will leave you 8% after their administrative overhead and periodic episodes of bad stock markets. Therefore, you must get over any prejudices against investing in common stock, and any dreams of getting rich by plunging in them. By passive investing in index funds of the entire American (or perhaps entire World) economy, you should really expect at least 12.5% return, fairly steadily. As can be seen throughout this summary, we have consistently under-estimated future revenue and overestimated future costs. Making 8% net out of 12.5% gross is not easy.

|

$132,000 in contributions, plus $218,000 at 8% compounded.

|

| Lifetime Revenue |

|

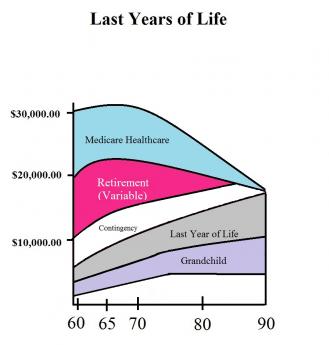

Expenditures: $200,000 Deposited:$8,400

|

| Medicare, Longevity 83 |

|

Expenditures: $308,000 Deposited:$6,000

|

| Medicare, Longevity 93 |

Financing Health in Middle Age. So, having between $187,000 and $297,000 to spend, what are the expected health costs for a middle-aged person? They will be quite moderate between age 26 and 55, starting to rise considerably in the last ten years, from 55 to 65. During all of this period, the individual will have to save $3300 per year, and in addition, will have to pay for obstetrics and pediatrics out of that. If children had any money, these costs would rightfully be theirs to pay. But children do have one asset to contribute: 26 years of additional compound income. In a theoretical sense, the children need to borrow their own medical costs from their parents. It might be said they should pay this back to their parents directly, but it is the grandparents who will be experiencing the rising medical costs of their fifties. By legally merging children and parents until the children are 26, a choice can be made between encouraging fertility and helping the kids with college costs or helping the grandparents with unexpected health costs. Ideally, it would be preferable to let the family unit decide such choices, but matrimonial courts are full of examples of family dissension, and quarrels between headstrong adolescents and their neurotic parents. It's only a suggestion, but it seems best to me to let the parents decide until the child is 21, and let the child decide after that. Invisibly, the quirks might have to be adjusted in the parents' wills and estates.

Financing System Shortfalls. There's one final question to answer. What if, for whatever reason, there isn't enough money in the system to pay all the legitimate bills? We can fumble around with eliminating fraud and abuse, but that won't make much difference. The government can be the banker, but someone might well have to be individually responsible. There is no escaping it, the extra money will have to come from additional deposit contributions by people with an income. Probably, extra deposits will have to be levied on people 50 to 65, who will be at the top of their lifetime earning capacity and beginning to experience a greater share of the costs. At that point, it may seem easier to repay the grandchildren costs by repaying the health loans of children to grandparents instead of parents. It could be done quietly by assessing extra deposits on 50-65 while shifting childhood repayments to grandparent accounts. Immediately, a much smaller amount could be deposited in the children accounts, where compound interest for 26 years would multiply it back to where it started.

Let's Do It All, Backwards. Children's healthcare is paid by the parents. In order to capture 26 years of compound interest, we try to unify the legal family until the child is 26. The child owes a debt, to be repaid to parents or grandparents, later. At age 26, the individual starts depositing $3300 yearly into a tax-exempt Health Savings Account, paying back at least 8% on passive investing in American or Worldwide index funds of common stock, essentially capturing a diversified share of the entire market. This HSA can pay health expenses, but those who can afford it would be wise to pay their medical bills out of other accounts and save the tax-free feature for bigger sums, later. A high-deductible health insurance policy pays big bills, the HSA can (but need not) pay the high deductible. This is how things go until the individual is 65, except between $150 and $325 is placed into an escrow, which will be used on the 65th birthday to buy out of Medicare. It's possible for the individual to deposit less, perhaps $3075 to $2975, but the alternative is to buy out of Medicare, a much better deal.

That's how it goes until the 65th birthday when Medicare appears. The working person has already paid for a quarter of Medicare's costs by payroll taxes. He now faces an equal amount as Medicare insurance premiums, as well as double that premium cost in federal subsidies, plus accumulated foreign debts for earlier subsidies. Right now, only the foreigners are worried about repayment of the debt, but somehow or other it has to be paid. The alternative was to have deposited $150 to $325 yearly, but now it will cost you $187,000 to $297,000, so for most people, it is too late. Meanwhile, the government has collected a quarter of Medicare's cost in payroll deductions, so it should owe you something for that, too.

Oh, yes. If you happen to have been unusually healthy, you didn't spend much money on health. All of that accumulated money is available to pay for your long, long, retirement.

The Big Picture

The main purpose of fitting a small picture of health financing reform, into a big picture of health financing, or even into a bigger picture of national financing -- is to help judge whether the proposed reform is even remotely feasible. In constructing this assessment, our first task is to see whether healthcare as we project it can be self-sustaining. If not, we would have to look around for something else to subsidize it, because healthcare is not going to go away. We would have to shrink its ambitions, or else shrink the ambitions of something else, like abolishing the rich in order to subsidize the poor. Therefore, balancing the books in this context means showing how the health system can become self-sustaining.

Revenue Let's start with available revenue, which must ultimately come from people of working age. That is to ask, how much can people from age 26 to 65 afford to devote to healthcare? Their children are too young to contribute, and after they retire, the retirees are living on what they accumulated while they were working. Everybody hopes to save a little more than that, but what they have is probably best put in the category of retirement costs. Other derivative savings categories, like corporate income and government subsidies, either come directly from working people as taxes, or indirectly from organized charities, inheritances, and savings. Since 1965, aggregate foreign transfers have all been negative.

Painless Augmentation of Revenue. All budgets seem to start this way. Everybody's appetite seems bigger than his wallet. But few budget discussions begin with the proposal that we perpetually find new sources of revenue for two-thirds of projected expenses. That is, most organizations assume you have to borrow in order to meet your goals. Eventually, you find new sources of revenue, or else the debt service grows to a point it destroys the vision thing.

Substitute Investment for Debt. We presently regard the diverging curves of revenue and expense as a tragedy, when they could be turned around as good luck. The pay as you go system allowed employer-based health insurance to forget about the early costs of people who had not pre-paid them. In a sense, pay-go borrowed its capital costs and never expects to repay them. It may have assumed later generations would pay off the debts, but the later generations just continued the minute, and let it grow. Like all insurance companies, it rejoiced in the gift of protracted payment periods, growing out of unexpectedly extended longevity.There's a tipping point in such developments: if the interest you earn on savings is greater than the interest paid to your creditors, your debt burden shrinks; if it's the reverse, you probably go broke. In the favorable case, the more longevity keeps extending, the cheaper it becomes to extend the debt. The health industry has permitted the insurance and finance industries to enjoy this windfall. It's time for the Health Industry to take possession of what it created, but you need not expect the insurance and finance industries to cooperate gracefully. As John Bogle so annoyingly pointed out, the finance industry has absorbed 85% of the income from investments. The insurance industry is allowed to charge 10% to collect healthcare bills. And big business finances the transfers by paying half of its inflated tax liability in taxes, while denying the same advantage to its foreign and small-business competitors. No one expects these three giant industries to roll over on command, but the government can be pressured to stay out of the road while the healthcare industry switches from being a debtor to being a creditor, hence avoiding bankruptcy in order to be rewarded for extending everyone's lifespan by thirty years. In short, by switching from pay/go to Health Savings Accounts. From debt-pay to pre-pay.

Substitute Independent Multi-year for Employer-based One-year Term Insurance. Since both the Clinton and the Obama health reform teams had extensive contact with business interests, there is little doubt they were well aware of two flaws in the employer system. It is not portable, leading to the campaign agitation about "job-lock"(Clinton), and it does not roll over from year to year, resulting in a furor about pre-existing conditions(Obama). These are both manifestations of employer control, inherently consequences of employment mobility. It is unclear what combination of pressures impelled both administrations and their political associates to avoid the ERISA solution of shifting employer control to an independent insurance company, funded by employers. Perhaps it was fear of union domination of ERISA plans, perhaps it reflected resistance from non-profit insurance, perhaps something else. In any event, this resistance stands in the road of the many advantages of multi-year coverage, perhaps forcing attention to inferior solutions less directly distasteful to employers.

In any event, the lifetime cost of whole-life insurance is roughly a quarter of the cost for equivalent coverage in year to year term insurance. Furthermore, the term product is generally less attractive as a revocable product, hence even more expensive than it seems. It is certainly troubling to hear that term insurance would be unprofitable if fewer people dropped their policies. We would defer to insurance experts on the relative merits of different ways to extract cash from them for medical requirements. Using the cash balances is one way, reducing the terminal benefit is another. Nevertheless, the HRA experience is only half of the accounts have any yearly withdrawals at all, so perhaps the whole-life approach contributes only half as much as its final balance to paying for healthcare. If it eliminated the need to prohibit pre-existing conditions, it might save even more. Perhaps whole-life and term would have appeal to different age groups, so the ability to transfer should be protected. The need to create an information and research center for healthcare is evident in questions like this.

Where Should the Retail Outlets be Located? Health Savings Accounts can be regarded as insurance plans with a banking front end, or else regarded as Savings accounts with fail-safe insurance attached. Instead of a fight to the finish, it is exciting to envision one plan as part of existing insurance offices, and the other as part of brokerage houses. The resulting competition might quickly surface important advantages to different customer needs. It might also adjust more easily to shifts from inpatient care to outpatient, or different state regulatory postures. Some thought might also be given to facilitating foreign medical tourism.

Zero-sum (Painful) Augmentation of Revenue. For health insurance to cross the tipping point between a debtor and net creditor, it must receive a greater return on its investments. The investment community is struggling with a recession and a hostile regulatory climate and will resist a loss of margin unless it is accompanied by a considerable increase in sales volume. They are entitled to make their case but are not entitled to make their own facts. The government needs to assure that prices are more widely transparent, and cost-free transferability is easy. Fees for deposits, withdrawals and transfers should be both low and immune to kick-back arrangements. Fiduciary status should be encouraged if not mandatory. Competition in the sunshine should be the goal, so long as investment income is comfortably above the tipping point. Health Savings Accounts already report $22 billion in deposits, while potential volume is a hundred times that much. There is room here for all participants to prosper, and for optimum rules to emerge. Somebody without narrow boundaries should be empowered to watch, to prevent, and to enforce. With some imagination, the Constitutional quarrel between Federal and State regulation could be turned to advantage, not to obstruction.

Balancing the Books. In this summing-up exercise, balanced books imply health industry self-sufficiency. Even if it is decided to unbalance them by, let's say, subsidies to the poor, the size of the subsidy should be measured against the size of the budget, and the size of the populations involved. Somebody or some agency must be charged with doing so, because health financing is very fluid.

As a first step, health savings Accounts at their most optimistic, fall $50-$80 thousand short of stretching $132 thousand into $350 thousand. That's a whole lot better than falling $200 thousand short, which is the present plan. Almost by definition, we don't believe it can be done by raising cash contributions, but it is sure one big step toward it. As data accumulates and the economy clears, we hope the figures will seem more favorable. As medical research progresses, we hope the overall costs will go down, but an expensive cure for cancer could blow that hope away.

We might expand the international trade of healthcare, both by sending Americans abroad where labor costs are lower and by importing foreign nationals for expensive forms of care, at a fee. For a long time, there was a weekly flight between the Netherlands and heart surgery in Texas, to the financial benefit of both countries. We have not made much effort in that direction, since that time. And finally, there has been very little progress in converting the infirmaries of retirement villages into low-intensity hospitals, an advance with considerable promise if helicopter transfers were facilitated and telemedicine advanced. Because of hospital zero-sum resistance, this trend would best begin in remote regions, and might even require some pilot studies. Finally, it would help a great deal if the retirement age spontaneously moved several years older. Perhaps to age 75. Beyond that, we are going to have to resort to subsidies and cost-cutting to balance the books. That's not the best solution, but it's all this approach can provide. By the way, that's not exactly peanuts. Try multiplying $100,000 times 340 million to see what an advance we have made on solving an apparently unsolvable problem.

If anyone is still listening, we seem to be forced to start experimenting with lifetime Health Savings Accounts. They have more promise, but less experience to back them up. Very likely, they might produce an additional lifetime $100,000 revenue, but they have one immediately important obstacle. We might very well find they cannot do what we want unless the nation is willing to surrender Medicare. No one needs to tell me the politicians regard that as political suicide, because almost no one is willing to face the fact we cannot pay for it, to the degree it is itself probably a bigger problem than the rest of the population's healthcare, and almost no one will face it. I won't repeat the mathematics here, but Medicare is 50% government subsidized. Think it over. Even I am forced by public opinion to soft-pedal the facts, hoping other people who have nothing to lose, will start to speak up.

"Scores of Centimillionaires"

John Bogle John Bogle is an investor with an evangelistic twist. He sold over 800,000 copies of his various books about Mutual Funds, donating the royalties to charity. One theme running throughout his writing is that no unmargined investment manager can focus exclusively on equities in his portfolio and expect to have a higher return than the index itself, whether he is an index investor, or is more activist as a portfolio manager. About five or ten percent of managers do beat the index each year, but they are general managers of small funds, and generally cannot repeat the performance consistently. It's a very useful message since the conclusion seems to follow that if a manager simply imitates the index, he will surely reduce his research costs, and will therefore almost surely have consistent final results which beat the average competitor. Ultimately, the best results will be found in long-term index funds with the lowest costs. That's a conclusion both logical and borne out by results; no amount of denial can refute the logic of it.

However, it is also possible to take it as a challenge. What approaches might be tested, to see if they can beat it? Mr. Bogle himself admits success might defeat a front-runner, by attracting so many investors the portfolio is forced to limit itself to large-size when the supply of frisky small stocks gets used up. If the small newcomers out-perform the blue chips, average big-fund performance will suffer by comparison with small boutique funds. Indeed, small-fund indices often display a 2% outperformance, compared with large-cap indices. It would probably be useful to consider closing a large fund to new purchases when the average size of its investment is forced to contract downward. Since such a reaction benefits the investors but not the managers, the right to close or reopen funds should be transferred to the shareholder investors.

Common Sense on Mutual Funds New Tools. It is common for mutual funds to limit or forbid short-selling, as well as buying on margin. That's obviously less risky than engaging in such activity, but most investors understand greater returns require greater risk. That seems to be the approach adopted by hedge funds, although the success of it is often shrouded in secrecy for good reason, and has nothing in common with other stockmarket talents like demanding high fees. The main limitation on hedge fund competition comes from the excessive fees (2% annually, regardless of profits, plus 20% of profits themselves, and a five-year lock-in.) In effect, such activities can be simulated by funds controlled by a single university or pension fund. A fund with a large float of incoming deposits can treat the float as a virtual loan, and an organization which needs to mortgage a large construction project can treat the construction loan on the building as a virtual mortgage on the stock portfolio. It might further be argued that other organizations without a stock portfolio are overweighted in fixed assets whenever they take out a mortgage. Closed-end investment trusts seldom leverage overtly, but they usually are sold at a 10-20% discount to net asset value, and thus are effectively leveraged. Warren Buffett, the greatest stock market manager in history, owes much of his success to buying an auto insurance company outright and then using its float from premium deposits as if they were part of his portfolio. He tends to buy entire companies; their dividends disappear. In special circumstances with 1% prevailing interest rates, it can be difficult to make the case that borrowing is too risky for long-term investments; the issue now is liquidity.

And one final warning. When too many people get overleveraged, by whatever method, they generally sense the approaching dangers but often are restrained from selling by the tax consequences they would experience. But when it looks as though everybody sees the same thing, there may be a rush for the door. It's called a crash. So don't you dare buy on margin? Let me do it, and together we'll blame the speculators.

REFERENCES

Common Sense on Mutual Funds: Fully Updated 10th Anniversary Edition: John C. Bogle ISBN: 978-0470138137 Amazon Finding the Sweet Spot

Every tennis racquet has a "sweet spot", a place within the stringed area that hits the ball just exactly right with minimum effort, and for that matter, does so with a minimum of noise. If your aim is good, the shot is much improved by whacking it with the sweet spot. In health savings accounts, the sweet spot is that combination of fixed choices over which you have no control, like your age, and independent choices over which you do have some control, like the amount you deposit into the account, or the shrewdness with which you choose your agent. There's a somewhat different sweet spot for males and females, and it will vary with the state of the stock market, or international warfare, during the era in which you had the highest earning potential. In other words, the cost of sickness is the only chance catastrophe we are aiming to protect against. For that narrow purpose, the uncontrollable factor which makes the most difference is

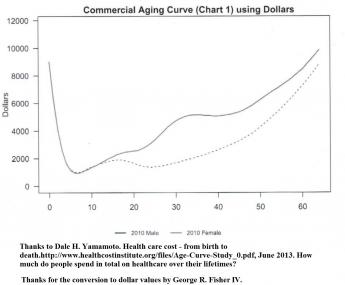

The age at which you started your spending account. Compound interest requires time to work; persons who start their accounts late in life no longer have to pay for their earlier expenses, but they must have some traditional insurance protection during the transition to full dependence on the account, or else some other form of savings. That's why you need catastrophic insurance coverage, but in the early stages of getting established, even that could be inadequate, and nothing can be offered unless the government offers to subsidize it. In order to find a way to capture twenty extra years of compound interest, it is tempting to begin depositing at birth, which is presently prevented by the HSA rule that you must be working to start an HSA. But children have health costs to be managed. In particular, 3% of all health costs are reported to occur in the first year of life. If Congress will allow it, we have a plan in later sections for doing it expeditiously.

Subsidies for the Unemployable, Such as Children. Please do not compare subsidy with lack of subsidy, because the subsidy is always cheaper in the short run. . Furthermore, subsidies are created by the government, and are therefore under pressure to demonstrate equity. Protection in extreme cases must rely on reasoning which placates the "Equal Protection" clause of the Fourteenth Amendment. All forms of insurance contain some incentive not to invest but to squander, and channeling that choice is part of insurance design. Here it attempts to balance a singular opportunity to select the best possible investment opportunity, with the unique ability to spend the proceeds on anything you choose after your health cost has been met. Unfortunately, we have already gone so far with borrowing for health, that many people are of a mind to believe balance can't be achieved. We could go on with this, but a quick summary is there are thousands of possible sweet spots, most of which are partly beyond anyone's control or ability to predict. There are even some circumstances where an individual would be better off putting reliance on Obamacare, trusting the government to bail him out with subsidies; if the nation decided to give equal subsidies for every payment alternative, however, most of these short-term advantages would disappear. The best we can suggest for people who dislike both HSA and Obamacare is, go see your congressman. In this book, we merely suggest that most people would be better off with HSA.

Trying not to be repetitious, there's nothing you can do about your age and sex, or previous state of health. You should have stopped smoking twenty years ago, but you can't help it now if you didn't. Twelve million people already have HSAs; if you aren't one of them, the best you can do is start one now. It's very difficult to imagine a situation in which a late start would inflict harm which subsidy couldn't help. On the other hand, if you make a bad choice of agency, make sure you are allowed to switch to a better one if you can find it. Some brokers charge too much, some of them pick poor investments to get a kickback. Some demand too large a front-end investment, although that may do you a favor in the long run. Essentially, your own choices affect the result, and your main recourse is to invest more than you planned. For the most part, the more you invest the better. If you invest as much as you can and it still isn't enough, you made an investment mistake. It's only a real catastrophe if you then get sick, and Congress didn't provide for those few who inevitably make such a double blunder. In that case, it will have required three misjudgments for a serious mistake to emerge, because even this mishap will be adjusted by aggregate subsidies costing less than the program is able to diminish overall costs -- a very likely outcome.

Interest Rates. Unless you are within a few years of death, or within a few weeks of a stock market crash, in the long run, you are generally better off with stocks than with bonds or money market funds. According to Ibbotson who published the results of all asset classes for a century, the stock market has averaged 11-12% total return for the past century. However, if you maintain internal reserves against a depression, you will probably only receive about 8% as an investor, of which 3% is due to inflation, so figure on a steady 5% after-tax, after-inflation return over the long haul. Use 8% as your shopping guide, resign yourself to 3% inflation loss, and content yourself with complaining about the 4% attrition seemingly imposed by the financial industry. You will find our charts use 5% tax-free as a standard, but show a family of curves up to 12%, just in case someone figures out a better system for harvesting the return. For 3-5 year depressions ("black swans" occur about every thirty years), we show curves of lower returns. Notice endowments and professional investors also figure on 5% overall from a 60/40 mixture of stocks and bonds, because they have a payroll to meet, but you may not. A conservative investor can feel comfortable with a 5% "spending rule", but that assumes a long horizon and the need to make expenditures. Some people have a short horizon and may be able to gamble on a pure stock portfolio because they have some other way to meet medical expenses up to the deductible on their catastrophic high-deductible insurance. But they better know they are gambling, and may, therefore, encounter a black swan they can't cope with. Such people probably need financial advice, because it is also possible to be too conservative if your deductible is comfortably covered. Fear of underfunding may cause the account to become overfunded, but that is scarcely a tragedy because you can withdraw your money without penalty after age 66. In fact, a policy of deliberately overfunding the account at all times never has any great downside, and lets everyone sleep better.

Age at Beginning an Account. If you begin to use an HSA during late working years, you have the consolation that you no longer need to plan for paying for the first forty or fifty years of your own health. However, the years of heavier medical expenses begin around age 45, by which time you have already paid for most of your Medicare payroll deduction, which is about a quarter of Medicare costs. The older you get, the more you have paid with a payroll deduction, but fewer years are left for compound interest to accumulate within the account. Balanced against this is the likelihood you are entering your highest earning years, which carried too far, may tempt you into unwise early retirement. You may need some accounting advice about what is best and still feasible. And you may need legal advice if the laws change.

Younger working people have contributed less to payroll deductions but have longer to earn compound interest in their HSA. People seem to have figured this out, and the largest group of new subscribers are in their twenties and thirties. This is the group with most to gain by proposing a buy-out of Medicare. A quarter of Medicare is paid for with payroll deductions, another quarter by Medicare premiums after you reach 66. If Congress could be persuaded to drop these contributions, what would be left is the half the government pays by borrowing from foreign sources. If you, in turn, agreed to pay off this indebtedness, the government might be tempted to match it by foregoing part or all of your payroll deductions and premiums. Since one about balances the other, the compound interest you earn on your deposits is pure profit. From the government's viewpoint, it might seem a great relief to know the debt would stop growing. Older people are generally so deeply committed to Medicare they would resist, but younger people -- and the Treasury Department -- would find it quite a bargain. Once again, financial advice from somebody good at math is highly advised. When the politics of this matter settle down, it should become possible to state a particular age, below which a Medicare buy-out is safely advisable for anyone. It's almost always in the Government's favor, so independent advice is only prudent. In summary, starting an HSA at almost any age is safe and wise. A Medicare buy-out is wise below a certain age, yet to be determined. In other circumstances, a buy-out is wise if personal finances are comfortable, but right now it would take financial advice to do it. And, of course, a friendly politician to convince Congress to make it legal.

There are two more steps to this transition. But before getting to them, it seems best to run dual systems while you phase one out and phase the other in. It may even prove to be best to run two systems indefinitely. Three principles emerge:

I. It would be pretty hard to run dual systems without also running subsidies for both. This would be part of Equal Justice Under the Law. It's hard to run dual subsidies until you know what the final rules would be. Some subsidies may be difficult to match, and require equivalent subsidies, which are harder to devise.

II. Dual systems and patchwork fixes always provide loopholes for someone seeking to take advantage. Some agency must be designated to keep this in line, using the principle of each system being charged with watching the other one. When you deal with one-seventh of the GDP, tremendous scams are entirely possible. A system of balanced whistle-blowing could effect great savings without the same surveillance costs.

III It isn't necessary to pay for everything. The reader will, of course, have noticed that paying for all of the medical care would save perfectly stupendous amounts of money. But paying for half of it would also save stupendous amounts. And even paying for only a quarter or a third of everything medical would save the economy two or three percent of Gross Domestic Product. That wouldn't be a failure, it would be a tremendous success. In fact, it might be all the change the economy could withstand for a few years.

The Intergenerational Roll-Over.

The Coming Shift From InPatient to Outpatient Care.

Steve Brill: Healthcare Without Insurance Companies

Stephen Brill Stephen Brill has written a very professional description of the "Inside baseball" of the Affordable Care Act, from the decision to go ahead with it, through the turmoil of ramming it through Congress, to the badly mismanaged introduction of the insurance exchanges. At the conclusion of this largely critical description entitled America's Bitter Pill , Mr. Brill devotes fifty pages to his own proposal for a better system.