6 Volumes

Constitutional Era

American history between the Revolution and the approach of the Civil War, was dominated by the Constitutional Convention in Philadelphia in 1787. Background rumbling was from the French Revolution. The War of 1812 was merely an embarrassment.

Health Reform: Children Playing With Matches

Health Reform: Changing the Insurance Model

At 18% of GDP, health care is too big to be revised in one step. We advise collecting interest on the revenue, using modified Health Savings Accounts. After that, the obvious next steps would trigger as much reform as we could handle in a decade.

Second Edition, Greater Savings.

The book, Health Savings Account: Planning for Prosperity is here revised, making N-HSA a completed intermediate step. Whether to go faster to Retired Life is left undecided until it becomes clearer what reception earlier steps receive. There is a difficult transition ahead of any of these proposals. On the other hand, transition must be accomplished, so Congress may prefer more speculation about destination.

Handbook for Health Savings Accounts

New volume 2015-07-07 23:31:01 description

Consolidated Health Reform Volume

To unjumble topics

(1) Obamacare: Spare Parts for a Book

Maybe these should have been included, but it was decided to leave them out.

Health Reform: Seen On the Mass Media

Both political parties in the 2008 election promised to revise healthcare financing and delivery; the nation was restless. It had been restless since a Republican Congress swept Newt Gingrich to Speaker in 1994. It soon swept him back out of power, but its ability to surprise reappeared in 2010 with Republican Senator Scott Brown's election to Edward Kennedy's seat, and then there was the 2012 Republican Congressional landslide, -- but on the other hand there was President Obama's 2012 re-election. One electoral mandate after another, often sending opposite signals. Only a King is allowed to be capricious, nations are described as undecided. When Democrat Barack Obama won his first election in 2008, a concrete proposal was eagerly awaited because it seemed likely to be radical; it disappointed because it merely overpromised. He neglected the iron rule for leadership: underpromise but overdeliver. In order to retain a free hand, the working elements of Obamacare were never concisely stated; in America, that is usually a misjudgment. After enactment, details can no longer escape systematic examination for what they are, and what they omit. We got rid of our King more than two hundred years ago. Capricious behavior is out of fashion. Over-deliver, that's the thing.

Political strategists calculate sweeping changes have the best chance of approval immediately after a new president takes office. But for the Affordable Care Act, that slogan may still have been true but mis-timed; since overly brief sequencing gave interest groups responsible for Obama's election undue influence over the proposal, with an undue sense of mandate from the elections they won. The resulting legislation, the Affordable Care Act, is heavily slanted toward rewarding the base, and the base expected a reward. With its momentum up, organized Labor, blacks and Hispanics displayed impatience about mitigating features the rest of the nation objected to. As Lyndon Johnson once said, the majority of Americans are non-black and non-poor. Political misjudgment increasingly characterizes Obamacare, which at first seemed so smart about politics..

Thousands of pages of uncoordinated proposals had emerged from four congressional committees in 2010, confusing the public about what the basic proposal was, and making it uncomfortably obvious that the congressmen themselves had neither written nor properly digested it. It was announced as a proposal to expand coverage to the whole population, uncharacteristically saving the resulting cost by eliminating waste and overutilization in medical care. That appealed to the public. But without more explanation about how these goals would be achievable, in fact, whether the premises were accurate, the public could not see how to program expansion and cost reduction were consistent, or how these two thousand pages made them so. Universal health insurance was said to be mandated, but in fact, it doesn't say so. What it says is everyone has a choice between insurance and a small tax. Anyone with a pencil knew what to do next.

Furthermore, the public could not see what urgency justified delivering a stack of paper to congressional authorizing committees in the morning and demanding an affirmative vote in the afternoon of the same day. Consequently, the conviction took hold that what was proposed would end up being a massive cut in Medicare benefits to pay for it. Soon after the voluminous bills were released, the Congressional Budget Office (CBO) further undermined trust in the proposal by announcing its assessment that it would add a trillion dollars to health costs in ten years, but still would only extend new insurance to about half of the uninsured population. That didn't sound like universal coverage at no added cost, at all. Furthermore, the CBO had credibility, in fact, was the only credible agency that had actually studied this massive legislation. The President immediately appeared on television, endlessly repeating the promise that the extra cost would not add one dime to the public debt. Therefore, fear of large impending Medicare cuts had to be entirely plausible if you believed anything the man said. The public uproar about an implausible idea thus became general before members of Congress had time to read it or devise soothing explanations; their floundering upset the public even more.

To rescue the deteriorating situation, the President attempted to go directly to the public with weeks of daily speeches. On one Sunday he appeared personally on five television talk shows. Naturally many speeches were ghost-written, containing misstatements or exaggerations, with the result that the harried President next resorted to heated oratory that would have been excessive even on the campaign trail. He was criticized as using rabble-rousing, undignified for a sitting President. Failing into a "trust me" approach, he actually was left with the difficult choice of withdrawing the proposal or being seen to ram it through Congress on a party-line vote. Party-line enactments of controversial legislation tend to justify the opposition party into repealing a controversial law just as soon as they return to power.

With the public bewildered as to what the proposal really was, enacting something certain to be reversed was even more unappealing. The alternative, a humiliating withdrawal of the proposal, seemed intolerable to its strongest supporters in the base. But reversal did not seem unreasonable to independent voters, who had wondered all along why there was such haste. The nation was fighting two international wars, both of them going bad, and was in the deepest economic recession since 1937. What's the hurry with this healthcare thing? It was a reasonable question, and the President did not help himself by darkly accusing opponents of delaying tactics.

* * *

In this analysis, the following three sections address 1) the proposal and its own flaws, particularly the savage strategy for getting enacted. 2) The growing consequences of flaws in health financing which had long pre-existed Obamacare and 3) An improved proposal, not so much radical, as extensive. For a century, conservative proposals of all sorts have been incremental, creating opportunities for mid-course corrections. Often denounced as hesitant and timid, a grand strategy often takes more time than a pitched battle, but usually advances farther and more enduringly.

Chicago Sauce on an Arkansas Turkey

Presumably, the proposers of affordable health coverage considered the approach of making it affordable through making it cheaper. Unfortunately, "affordable for every American" is so expansive that some people, somewhere, would require extra subsidy no matter how much prices were cut. Obamacare's supporters would be bitter to discover a two-class system, with them in second class. It did not take long to see how unpopular cutting existing programs would be, first with providers and then with provides. And then Obama advisors must have developed a greater understanding that existing internal hospital cost-shifting meant: Medicare was already subsidizing Medicaid, while the private sector had really been subsidizing the indigent care that Medicaid excluded. The savings to government costs (of universal coverage) were not going to be nearly as much as had been imagined.

So, a subsidy program was required. In addition, ensuring illegal immigrants during high unemployment was seriously unpopular, particularly in border states like Texas, where uncompensated care was already hard to manage. So we can easily imagine how the proposal emerged as: "Affordable health coverage for all Americans (legal residents only) achieved by giving cash subsidies ("refundable tax credits") to lower income groups, and expanding Medicaid coverage above its former income threshold". That wouldn't be a catchy political slogan, but it would be precise.

Such patchwork necessarily made it harder to comprehend. Somewhere in its evolution someone also seems to have determined to rescue Medicare from its impending bankruptcy -- while we are at it, let's fix Medicare. However both ideas, universal coverage and restructuring Medicare solvency, would be expensive; combining them might make the package unsupportably expensive in a recession, but it might also create more opportunity for major progress.

Affordable health coverage for all Americans (legal residents only) was to be achieved by giving cash subsidies ("refundable tax credits") to lower income groups while expanding Medicaid coverage limits to include them. A universal mandate for coverage, (but only our way, or the highway.)

|

| Obamacare Capsulized |

The Obama administration seemed to follow the same path. Modifying the pathway to a Budget Reconciliation Committee added the novel advantage of avoiding the Senate's 60-vote anti-filibuster rule, thus requiring only a simple majority to pass the Senate when it returned. It still needed 60 votes in the Senate to prevent a filibuster on the initial round, so the original Senate contribution to the conference committee had to contain a lot of goodies, just to get to the conference committee -- in order to be dropped.

In the flurries of lobbying activity, hospital advocates have suggested uninsured patients just appeared at hospital accident rooms, effectively causing other patients to subsidize them. That was somewhat true, but extending the idea to a claim the government was already paying for all indigent care, was a stretch because hospital cost-shifting was laying most of the cost on the private sector. To go further and proclaim that including indigent care under the insurance coverage umbrella would thus be cost-free, did really strain the facts. How could it be cost-free and still cost a zillion dollars? Right from the start, this proposal was making itself hard to defend.

|

The sound-bite is: the Obama health reform proposal of 2009 will extend affordable health insurance to poor Americans (citizen), and save Medicare from ruin by cutting costs. Because this still won't pay the bill, the rest of the nation must get less coverage for more cost.

|

So, at the end of September 2009, the country confronted multiple thousand-page bills from the House of Representatives containing wide assortments of liberal ideas, and a more conservative Senate proposal from Senator Baucus (D, Montana) representing the views of the Democratic caucus within the Senate Finance Committee. The British magazine The Economist promptly snorted; Senator Baucus' bill was "Half a loaf, half-baked." Since laws passed by strict party votes are in danger of prompt reversal when the other party next gains majority control, Senator Baucus had been struggling to achieve some Republican support but apparently decided bipartisanship was not worth the delay. In any event, the Senate's assignment was to get past a filibuster; the real zingers could come from Nancy Pelosi's House bill. Andy Stern the labor leader, had appeared on a television show offering no arguments at all, merely demanding a vote be taken instantly, presumably before public support eroded. Moderate House Representatives are characteristically most concerned with being turned out of office after passing a controversial proposal because they face election every two years. The much more liberal leadership of the House, with seniority because of their safe gerrymandered seats, are however more likely to honor extreme partisan demands. With a safe Democratic majority of the House, a few moderates could be spared to "vote their conscience".

Because the Senate thinks of itself as the sensible, deliberative body, oversight of law remains with its originating committee, to preserve the connection to the "intent of Congress". Because Medicare and Medicaid are amendments to the Social Security Act, the Senate Finance Committee has maintained jurisdiction over these three social benefit programs. A "unified budget" made it easier to shift one program's surplus to cover another's deficit. In the House, with turnover every two years, continuing oversight is mostly assumed by the Appropriations Committee, on the grounds that this is the only committee which reviews every ongoing program, every session. But the realities of the program mix with the quirks of the Senate, and for over forty years whatever the Finance Committee says about Medicare, pretty much goes. During the fall of 2009, this group of old colleagues could be seen on C-Span, gently joshing each other, and even more genially suggesting their disagreements. Each member of Finance belongs to several other committees, but on Medicare, they know their stuff and have a loyal staff to remind them of what they have forgotten. They considered 550 amendments to Obamacare, and stubbornly defended the right of each committee member of either party to be heard courteously, in spite of what must have been a wild frenzy of pressure by unions and other partisans, to be done with it. Their patient labors turned up one issue that party leaders -- especially the Governors -- probably wish they had left alone.

|

Blow away the smoke. Obamacare is about fixing Medicaid without admitting who, or what, caused it to need fixing.

|

| The nut of the matter. |

The fifty Medicaid programs are a big mess. They are run by state governments with Federal provision of at least 57% of the funds, and in some cases over 80%. Some states offer eligibility to those with incomes at only half of the poverty level, others go to several times the poverty level. Their tendency is to use the HMO model of healthcare delivery, but it is an individual state option. Minority groups absolutely hate HMO. The fraud level in Medicaid is by far the largest in the whole government. The quality of care is uneven, but it is always going to be somewhat substandard since it pays well below cost and deals with high-crime populations, amid uncomprehending chronic poverty. It attempts to deal with the deplorable psychiatric inpatient problem, which is in its present condition because of bungled regulation. Medicaid under-reimbursement is the main cause of hospital cost shifting, which causes still other distortions. And so on. If you search for an explanation of the bizarre statistics on infant mortality, the ranking of U.S. "health care quality" as 19th in the world, etc, the explanation is to be found right here. To the extent that statistics are not rigged in order to make certain countries look good, the poor rank of American healthcare reflects the sadly underfunded Medicaid programs.

Even the medical profession is largely unaware of Medicaid issues because most members of mainstream medicine have long stopped accepting membership in the program, in part because of its laughable reimbursement, but more importantly, the HMO organizational model makes it impractical to treat an occasional poor person free of charge and skip the paperwork. It, therefore, is sometimes true that some Medicaid physicians see nothing else. And finally, hear this: Senator Grassley muttered that 90% of the cost of Obamacare is aimed at fixing Medicaid, and no Democrat on the committee corrected him. When you get down to it, Obamacare is a very expensive program for making Medicaid what it ought to be, and definitely isn't. Originally confined to Maternal and Infant Care, its money is largely spent on nursing homes. This would make a perfectly plausible explanation for why it has been so hard to see what the new proposal is all about -- it's about fixing the old mess which state and federal governments created, while at the same time hoping to extend a similar program to the rest of the country later, as a "single payer" system. Senate Finance has a difficult tap dance with this one, but they have put their heads down and are plodding on.

|

Eighty percent of the cost is devoted to fixing the flaws of Medicaid.

|

| Senator Grassley |

Many unexpected developments are still possible in an on-going debate, but it seems timely to examine the Obama proposal as presently visible at half time, so to speak. What is so far proposed of consequence, and what problems would be cured?

Employer Mandates. First, nearly universal health coverage hopes to be achieved by mandates, making it illegal not to be covered, imposing fines for non-compliance. It does not seem extreme to predict a rise in the fines to a level where they support the rise in costs they provoke. That would serve the initial problem of pacifying the public during the early going, but ultimately justifying the Supreme Court assessment that it was a tax, not a penalty. Unfortunately for this idea, Justice Roberts stated in his opinion that the fact that the penalty was so low proved it was a tax. If the penalty tax was raised enough, it would prove it was not a tax, and therefore the universal mandate would become unconstitutional because the rest of the Court had already agreed that the Commerce Clause did not support it. Chief Justice Marshall once opined that "The power to tax is the power to destroy" which generates the justification that only a small tax is safely small enough to be a tax and not a penalty. It follows that while the Constitution permits the Federal Government to tax for revenue, it is not an enumerated power to tax in order to coerce or destroy. Justice Roberts may have been tipped off, but if not it was a shrewd guess.

Obamacare closes the safety valve that just about every poor person has long been eligible for Medicaid, but few of them actually join it until they get into a hospital and the social worker signs them up. The true antagonism of poor people to "Welfare medical treatment" has yet to surface into public view. Mandates are always unpopular, but back in Washington two competing ideas for mandates once headed for a conference committee. Because of the tax preference for the purchase of health insurance by employers, we still have a largely employer-based system, defining for poor people what normal health care looks like. As hospitals (responding to the shift of Medicaid costs to Medicare which they are forced to make) have increasingly shifted the costs of indigent care onto employer-based insurance, those employers who participate are increasingly anxious to make their competitors stop evading "their share". Unfortunately for this proposition, the non-participating employers never agreed to subsidize someone else, and do not feel bound by any moral strictures surrounding the demand of big business that their competitors are obliged to share a burden which big business decided to assume for its income tax benefit. If you doubt that small business and big business are competitors, just ask yourself what small retail businesses probably think of Amazon and Walmart. Then ask yourself whether very many small businesses benefit from ERISA.

Since almost all interstate employers already buy insurance for their employees under the coverage of the ERISA law, representatives of large employer groups want their competitors, especially foreign-owned, to experience equal expense. Big employers would thus be pleased with an employer mandate: employers who do not provide employee health benefits would be fined. Big employers are not so much threatened by little ones, as anxious to avoid government regulations which ultimately favor smallness as a preferred business model. By contrast, small employers are resistant to the employer mandate, amplifying the political perspective that increased cost would particularly hurt new employment in the present recession. Small employers enjoy and would hate to lose, the reputation of being the largest source of new jobs in our economy. Employer mandate might indeed ensure some uninsured people but the remaining uninsured would be unaffected. An employer mandate solves some purposes of big business but probably injures small business to a degree offsetting the cost-shifting argument. So, although an employer mandate was on the table, Senator Baucus proposed the individual mandate which Representative Pete Stark of Berkely, California had been advocating for years. That is, every person found without health insurance would be fined. Recall now, that Chief Justice Roberts introduced the qualification that the fine must remain small to be called a tax. Presumably, compliance would be even less than the widely-evaded mandate for automobile liability insurance.

One cannot leave the subject of mandates without the impression that there is some poorly understood connection with the Henry Kaiser income tax preference for employers who provide employee health insurance. Almost nothing can illustrate the intensity of warfare between big business and small business than this. Large employers definitely do not want to share this benefit with their smaller competitors, and definitely, do not want to say so in public. To the rest of the public, big business is taking the wrong side of the fairness argument, to say nothing of the Constitutional argument about equal treatment. But there is no other source visible for the seventy-year defense of the indefensible which has long convinced Congress that the tax inequity is politically impregnable, and cui bono will have to suffice. As long as this remains the case, there is some hope that some Congressman will be willing to fight it out.Individual mandate creates a somewhat different political problem of what to do about recalcitrants who are both sick and uninsured, who must now fear punishment as much as their illness when they appear for treatment. They are unlikely to forget which congressman voted to create the vexing outcome of fearing-to-seek-treatment. The Congressional Budget Office summed it all up: we started with forty million uninsureds, but it is most likely we will be left with thirty million uninsured (and now resentful) persons, including 7 million who are in jail, an equal number of mentally retarded or disturbed, and 11 million illegal immigrants. The very vocal remainder is hard to classify and hard to count. But the CBO is probably right, it's hard to see how insurance reform of any description will get the number much below 30 million.

|

Give the tax exemption to everyone, or give it to no one.

|

A second difficulty with the individual mandate is that it exposes the long-standing inequity in the Henry Kaiser tax law. The main reason we continue a largely employer-based system is that purchase cost is effectively reduced by the tax discount when an employer buys it for an employee. Self-employed or unemployed persons do not now receive this tax-discount. For seventy years it has been desirable to extend this tax exemption to everyone equally, both for fairness, and to create portability mitigating the pain of pre-existing condition exclusions. Pre-existing condition exclusion always existed, but it is the linkage to portability between jobs that makes it such a wide-spread issue. But the employer-based system might lose its main reason to continue, so that particular consequence has yet to be addressed. Inverting the traditional relationship between being sickly and paying higher insurance premiums has never sounded completely plausible, but we are now going to see what happens if we try it that way. Additionally, the political consequence of not equalizing the tax preference would get worse. Compelling millions to buy individual insurance, while at the same time denying them everyone else's tax exemption for it -- is not likely to survive long once it gets public attention.

Give tax exemption to everyone or give it to no one, or give it for a lesser amount, but give the same thing to everyone if you hope for re-election. While tax equity is not in the current legislation, it might as well be, and the CBO should be asked to score it as part of the eventual cost. And finally, no mandate in sight during a recession would insure illegal immigrants, who are a large part of the uninsured problem in certain regions. It is reported that sixty percent of uninsured persons are concentrated in Florida and the four states bordering Hispanic America, a fact that ten senators and several dozen congressmen are sure to notice. Proponents of amnesty for illegals have undoubtedly thought about this matter. Opponents of amnesty are apt to see immigration reform as just a way to cloak the costs of Obamacare as an unrelated issue.

Now turn to the other main objective of reform legislation, to reduce the high costs of medical care. The poster child of this objective, possibly the central issue agitating many politicians, is the approaching bankruptcy of Medicare. To skip over technicalities, accumulated subsidies of fifty years of Medicare recipients have created unfunded liabilities that make Medicare the largest single debtor on the planet, unless someone wants to compete with $250 billion a year. If you think about it, Medicare would have no debts at all if it were self-supporting. Until something is changed, the fifty percent subsidy of Medicare by borrowing from general tax revenues is steadily making the problem worse. The understanding of the public is just beginning to realize that Medicare is so heavily subsidized, and this is probably the main source of its popularity. Ignoring how this growing debt was created, it is accompanied by fifty years of promises to every citizen about what they are entitled to. Perhaps it was believed that an uproar over reducing Medicare benefits could be softened by burying it in a nationwide reduction of all healthcare costs, but half the cost of Medicare is a pretty big nut to bury, and fifty years of accumulated debt is just about impossible to hide.

In fact, such expansiveness provokes more suspicion that something is being slipped in by the back door. In angry town meetings which frightened congressmen, held during the August 2009 recess, one speaker after another went to the microphone and said something like, "I have excellent health insurance and I wish everybody else had it, too." Following which, something was immediately said equivalent to, "But don't you dare take my good coverage away from me to give it to someone else!" And not invariably, but often enough to make it emphatic, some would add, "I voted for you in the past, but I'd never vote for you, again." No doubt, every one of those congressmen was asking himself how the party leaders could have got him into such a fix. Why don't we try something else? Senator Baucus offered to pay for reform by putting a tax on health care providers, but every worried citizen quickly saw that taxing providers will raise costs, not lower them. Credibility is waning.

|

The Affordable Care Act would cost a trillion dollars, and still, leave 5% of the population without insurance.

|

| The Congressional Budget Office |

An adage is getting hardened: Increasing access to subsidized health care is not compatible with cutting costs, and won't even produce universal coverage. It is increasingly difficult for presidential oratory to reverse that opinion. The Congressional Budget Office has not pronounced the Obama plan to be an unachievable goal, but after examining an enormous pile of studies, it amounts to that. They simply said it would cost a trillion dollars, and would still leave 5% of the population uninsured. In one sentence, the CBO probably killed a lot of strategies.

Still, the Obama administration gamely plunges ahead, seemingly forgetting that defeat of the Clinton health plan was followed by a mass eviction of incumbent congressmen; by their analysis it wasn't a bad plan that made trouble, it was failure to pass the bad plan, which it must be recalled was a universal HMO system. The Clintons avoided public defeat by pulling that legislation away without a floor vote. But at least they did escape the backlash against what would then have been a ruinously unpopular program. It is not unrealistic to surmise that Obama would never have been elected to a first term if Clinton had not backed away from his version of healthcare reform. Right or wrong, some Democratic congressmen are certainly toying with that heretical idea.

For one thing, the public has always been bewildered by the need for such a rush, such a collision. We are now fighting wars and struggling with the worst depression since 1930. All of those major projects are going poorly. Why in the world would we believe that reforming health care is our major priority, right now?

The following section closes the discussion of the main features of the Obama plan and ignores thousands of pages of legislation not yet implemented. The law is mainly made up of earmarks, boondoggles, and in consequence -- the usual contents of an annual budget reconciliation act produced at Thanksgiving or the day before Christmas. We hear nothing about tort reform, which at most will produce a study or a pilot program. Nor the public option, which Senator Baucus said cannot pass the Senate, and about which former Senator Dole said he heard, but scarcely would believe, that the Public Option was just a smokescreen intended to distract the public while the rest of the bill slipped past the uproar of Public Option getting defeated. The fate of the expensive but inconsequential computerized medical record would once have depended on the precarious health of Senator Byrd of Virginia, who had long held a stranglehold on government computer procurements, but which now mainly perplexes us as to what to do with it. Blue-sky yarns about the value of the Electronic Medical Record abound. But except for large group practices which do seem to need it, most doctors see EMR as an expensive way to add two hours a day to their already overloaded workload and badly compromise patient privacy in the process.

How to spend

------------------------------------------------------------------------------------------------------- Throughout this discussion of the design of Health Savings Accounts, lifetime version, we have attempted to follow the underlying design of what we already do. That is, parents usually pay for children, old folks usually pay out of savings. So, once the money is in the Account, we try to imagine how it is now usually disbursed for healthcare, and even occasionally what the sources of it are. Our general choice is to follow established patterns where we can. Nevertheless, we favor debit cards in place of insurance claims forms, for all outpatient claims which fail to trigger the re-insurance deductible. Paying 10% for someone to pay your bills for you, is just unacceptable.Children almost always have their medical bills paid by their parents or their parents' insurance. Where to place the upper limit on childhood is a puzzle, but recent law has included children up to age 26 on their parents' health insurance. Since that seems to meet general approval, we adopt it, although it might be wise to allow emancipated children to opt out. Regulations on the use of parents' HSAs for their children are a little unclear, but we assume they would be easily changed if they conflict with reasonable practice. That parents-pay-for children system does complicate a smooth estimation of the future growth of the parent's Account, however, particularly in the event of a divorce of two parents with such accounts. It also interferes somewhat in the child's future right to claim compounded growth, so there is a brief temptation to give it to all three at once. However, the deposit was only one deposit.

In some ways, it is easier to have both parents contribute to the child's one-time initial deposit, in order to have longer for their compounding to continue, and to have the child's account begin with their contributions. This makes a $150 contribution at birth become $300, and you really can't keep responding to problems that way, without destroying the universal appeal of the plan. However, it is easier to imagine acceptance of double contribution with a later rebate of half of it, than to imagine a single contribution later cut in half. Perhaps it is easier to give people their choice of the two approaches, but it certainly muddles future projections. We opt for double contributions, with an optional rebate of the half at the child's 26th birthday, if the parents have had a falling out. With double contributions, there should always be a small surplus in the child's account, whereas sharing even minimal deficits is apt to cause more trouble in an already strained marriage. Double deposits as a default, single deposits as an option. Optional rebate at child's age 26.

Immediately we must expect an outcry about poor mothers who can't afford it. But every other proposal suggests a government subsidy for this purpose, and so do we. The ultimate savings to the government of putting up $150 per baby, would be enormous, but they would not be totally realized until the child was forty, and the government would be "loaning" the expenses in the meantime. An important reservation is the health expenses of the indigent are usually higher than average, obscured by the fact that many of them are not paid.

Grandparents. Children are repaying a debt to their parents, which parents frequently forgive; the parents initially pay it out of their own accounts. With the elderly, there are often no children or grandchildren; the elderly either have some savings, or they are indigent. Where there are descendants, they are not always willing to back the defaults of the elderly. If they bought out Medicare (with roughly $40,000, adjusted) after attaining age 65, they will, in summary, stop paying Medicare premiums, pay outpatient costs with a credit card, and their catastrophic insurance will pay the hospital an updated (we hope) version of the Diagnosis Related Groups (DRG) for inpatients. To adjust for contingencies the insurance might make a deposit in the patient's HSAccount for other medical costs (ambulances, for example), which the patient pays by credit card. Emergency care may well fall into this ambiguous category. The catastrophic insurance company is expected to have negotiated reasonable charges with the hospital, and to defend the patient against unreasonable ones. Rent-seeking in the outpatient area is more the patient's responsibility to detect, to object to, and to negotiate below a certain amount. Generally, the principle sought is to assume no responsibility for recognized overcharges, unless they have been agreed to in advance of the service.Working people, age 26-65, and/or their employers. At present, much of the health care of working people are voluntarily paid for by employers. Therefore, it is their choice what to do about a diminishing cost, absorbed in this system by their employees. Since the source of most of this windfall is an investment in the stock of their companies, perhaps everyone will benefit. Time alone will answer that issue, and perhaps it is too early to be making decisions about it. So for the moment we abstain from the fairness issue and do not greatly object to a gradual adoption of the HSAccounts for Lifetime Health Insurance, which is inherent in making it voluntary. However, it is clear that the employees are often spending for what they formerly got free, and as a beginning might well be gratified to have a roll-over of their Flexible Spending Accounts into Lifetime Health Savings Accounts. That would require the passage of no law, and perhaps ought to be requested politely. A surrender of industry's stance against income tax equity on health expenses would be nice, even though the Editorial Page of the Wall Street Journal cautions restraint in this effort, even restraint of the Tea Party members of the Republican Congress. I'm afraid I disagree on this significant point, which seems to put me to the right of the Tea Party.

That would seem to leave working-age people paying for themselves, their children, maybe their parents, and the indigents. Before that, for many of them, it was once all free. With that description, it is natural to expect some grumbling. But the cost to them is only a fraction of the former cost to the nation, and they get a great deal more control over an important part of their lives. It must be obvious that the old way was too expensive to continue, and it won't continue long. If for no other reason, unions will demand that everyone else feel some pain. Working-age people will end up with a bill of thirty or forty dollars a month, an undisturbed medical system, and no more yearly health insurance premiums. The employer has the employee health insurance cost gradually lifted from his back, and know very well that he will be pressed to spend some part of it for employee costs. Let him pay some into the HSAccounts, particularly during the early transition stage, when there will be very little investment "cushion".

And finally, it must be pointed out the federal government has been supporting a lot of this cost for nearly fifty years, but their instinct is to hide it. Fifty percent of Medicare costs are paid for with general tax money, quite effectively concealed in the budget term "Transfers from the General Account". Borrowing from foreigners is largely traceable to this source, and no one can be sure what will happen to world finance if it stops. Because this fifty percent subsidy would have to be extended to every citizen if we adopted a Single Payer system, even extreme liberals hesitate to press that solution, or imaginary solution to our problems. For now, leave it alone, and see how things are progressing.

Premiums and payroll taxes* Catastrophic Insurance= Debit Cards* Revised DRG= Personal funds* Direct Marketing= Internal loans* Escrow funds* Federal Reserve monitoring and midcourse adjustment. Deliberate overfunding of HSA*Data Sources for Health Care

OTHER REVENUE PROVIDERS WITH POTENTIALLY USEFUL MEDICAL DATA, MOSTLY UNUSED

Although some research discoveries are stumbled on by accident, most of the important ones derive from asking the right questions. If you don't ask the right question, you can wander around in a laboratory white coat for a lifetime without discovering much that is worth knowing. We already have huge stores of data, much of it in electronic form, about the health system. It mostly comes from people paying bills:

Health Insurance

Health Savings Accounts

Payroll deductions for Medicare

Medicare premiums

Military Medical Systems

Veterans Administration

Government subsidies to Hospitals

Medicaid (50-70% Federal)

Social Security

Life Insurance

Premium Investment Income

Cash payments (weak source)

Unclassified Remainder

To summarize the data sources already in existence raises questions of privacy and overwhelming government intrusion into the lives of citizens. That might well be a threat in forty or fifty years, but the disaster of the Health Insurance Exchanges trying to use a small particle of this data is reassuring, in a discouraging sort of way. These systems were originally devised to ask questions of no great relevance to national health costs, so they pose no great temptation to a wandering medical snooper. But they almost always have to meet some sort of an annual budget, so the answer to the question we are now asking is mostly available to everybody, on the Internet. It should be comparatively easy to learn, with adequate accuracy, how much is being spent on what kind of person, right now. If the total comes anywhere near 18% of GDP, we have as much detail as we need for this book to defend the conclusions it draws. We can tell the gross amounts, and by dividing by 350 million, get the average per person costs. Apportionment by age is somewhat less precise, but the numbers are so large, age stratification can be fairly accurately estimated. Let's start with a question we think we know the answer to.

Direct Marketing of Health Insurance?

New blog 2014-01-07 21:29:34 contentsWelcome to Welfare

|

Percent of Their Hospital Cost Reimbursed: Medicaid 70%, Medicare 106%, Private Insurance 150%, Uninsured 400% (?)

|

| Hospital Cost Shifting |

There's lots more; in politics there always is. The Pew Foundation, which now includes public opinion polling in its tasks, has pointed out 80% of the public does not share the polarization now so blatantly agitating the political class. Hence, some commentators have questioned the prevailing opinion of gerrymandering as the main source of it. These observers point to a worldwide decline in party affiliation; "independence" of party affiliation is claimed by nearly half of American voters when asked. Perhaps we have things backward, and gerrymandering is merely one effort, along with growing dependence on financial contributions by wealthy donors, to rescue party power. Television (and especially the Internet) prompts the voter to hang back before making decisions, hoping to decide something without pressure from party leaders. The growing tendency to vote straight party ballots is not taken by a few commentators as evidence of true voter wishes, but rather as evidence of the futility of resisting a two-party system. Some sophisticated observers feel straight ballots result from plurality ("first past the post") counting of votes, but this (unfortunate) trend seems more likely to be stimulated by (too) early voting by mail.

Since a two-party system favors moderate candidates over extremist ones, it may not be a bad system, but rather a good system adjusting to circumstances. A hidden cause of the present crisis in health care financing comes from the Medicaid programs, run by the states, but mostly (and inadequately) financed by federal taxes. A two-party system disciplines the nominating process by raising doubts about the ability of extremists to win the general election. Consequently, the final two candidates are often so similar the chance of a loser bolting the process, becomes small. In a proportional voting process, splinter parties cannot be silenced in the primaries, because political deals take place after the election when the public has become irrelevant to the voting outcome. Threats of public disaffection are therefore disregarded. This hidden feature went unrecognized at the Constitutional Convention, as indeed was the whole party apparatus. But it has to be counted as one of our greatest strengths, placing a much higher value on unity than dogma. If you follow this reasoning, you would have to conclude the present level of divisiveness will not persist. Because each generation has to learn its own lessons, it may recur, but it will not persist.

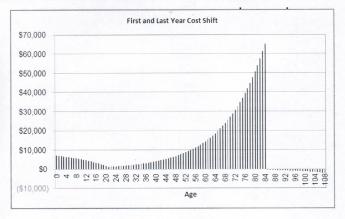

Nursing homes were not originally included in the 1965 legislation, but most states receive strong pressure to pay for elderly indigents in nursing homes, stranded by running out of savings. Perhaps it would be a good thing to include nursing home coverage in a reform bill, but nursing homes bear too much resemblance to work-houses to generate much demand to be in one. In variable degree, the circumvention has grown up of paying for nursing homes with money intended for hospitals but necessarily underpaying the hospitals. The hospitals make up the deficit by overcharging for outpatient services, as everybody will recognize who has been charged for the same service, both as an inpatient and an outpatient. By prevailing estimates, the Medicaid programs only pay hospitals about 70% of their actual costs. Hospitals escape insolvency to a minor degree by raising reimbursement demands on Medicare (to about 106% of costs) and more appreciably through private insurance (to something approaching 150% of costs). Teaching hospitals have some opportunity to raid funds intended for indirect research overhead, for resident stipends, and for disproportionate shares of an indigent, "self-pay" patients. Various accounting tricks account for the rest. For example, the transfer of schools of nursing from hospitals to universities has emboldened universities to seek the equivalent of traditional hospital reimbursement schemes, merely and mostly triggering new arenas for dispute, because the hospitals had hoped to profit from the transfer. Since Medicare somewhat overpays hospitals for its own patients, in recognition of the underpayment by states for indigents, current jargon blames the "government programs" for underfunding hospitals. A better summary of the situation is: Medicaid under-reimbursement is the largest source of hospital financing problems, but other problems are less resistant to change. That's pretty significant, in view of the Obamacare plan to put millions of uninsured into Medicaid, some of whom never asked to be insured at all, and most of whom have no previous experience with "welfare", so they need to start reading some books by Charles Dickens.

|

| Governor Christie of New Jersey |

The outcome of all this is nursing homes are in effect supported by Blue Cross and other private insurers of younger people, raising premiums to employer groups and individuals by something estimated like $900-1500 a year per subscriber. That's because Medicare is busy subsidizing Medicaid's hospital patients, the main source of hospital deficits. Because this juggling lacks straight-forwardness, results are inefficient; only about 42% of hospitals actually break even. As might be expected, knowledgeable employer Human Resources departments and hospital administrations know about and object to this system. They are cooperating with Obamacare more than might be otherwise expected, probably in the hope this cost-shifting can be adjusted more in their favor when it is less in the public eye. Mandating all employers to participate would, of course, increase the base of people sharing this exaction, but would ultimately link corporation treasuries to government deficits. The dream of the service unions would be to use this excuse to mandate the unionization of hospital employees. Governor Christie of New Jersey quickly saw a way to split the Union movement into public and private compartments through this. "Every time they get a raise, you get a tax increase," he told the unions of the private sector.

The participation of physicians in the Obamacare effort is riven by their own politics. For surgeons, the premiums for Malpractice insurance can sometimes run to $200,000 a year. An appalling proportion of obstetricians have been sued by their patients, to the point where women have no doctor to deliver their babies in certain parts of the country. For doctors in this high-risk category, relief from the plaintiff lawyers is the most pressing of all problems. On the other hand, many physician specialties have almost no malpractice risk and are much more exercised about the SGR reimbursement freeze, which has been in effect since the administration of Lyndon Johnson and has been severely undermined by inflation ever since then. With physician ranks divided by two different priorities, the way is open to promise both and reward neither.

|

The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.

|

| Tenth Amendment |

Urban-rural differences remain important in health care. Senators Baucus, Grassley and Snowe come from sparsely settled states. Former Senator Daschle is from South Dakota; there are perhaps twenty states potentially in this category. With a sparse population, it is difficult to develop sufficient insurance business for the law of large numbers to establish actuarial safety; these states need to combine into regional areas to reduce the competitive size of their loss reserves. On the other hand, populous states like New York, California, etc. are often adamantly opposed to regional groupings, for opposite reasons. These population disparities create differing attitudes about modifying the 1945 McCarran Ferguson Act, which limits federal insurance regulation and enables state regulation, thereby making it difficult for small states to agree to interstate health insurance sales and portability. The fact that large employers have already achieved this freedom through ERISA also makes them unwilling to see the problem or waste political capital achieving it for others. And thereby diminishes the power of low-population states to resist national healthcare insurance, which is their natural position.

And finally, Obamacare raises some questions about judicial remedies. Certain Op-Ed commentators have raised a question of the constitutionality of federal mandates or pre-emptions of state laws, depending on how they are phrased. The U.S. Constitution was only narrowly ratified in 1789, in large part because the states were fearful of the federal government getting bigger and more powerful than necessary. In response to this strong feeling, the Tenth Amendment reinforces in no ambiguous words, that anything not specifically assigned to the national government is to be in the province of the state or local governments. If ever there was original intent, it was that one.

REFERENCES

| Never Enough: America's Limitless Welfare State | amazon |

Co-Insurance (2)

New blog 2013-07-01 16:26:04 contentsIt's a convenience for the insurance company perhaps since it reduces the insurance cost by 20% and is easily figured on the back of a salesman's envelope. Therefore it helps in the three-way negotiation between the employer, the insurance company, and the union. The union calculates how much income tax the employees save by how much income is split between the "fringe benefits" (non-taxable) and the "pay packet" (taxable), and the negotiations shift around these offsets, usually at the end of grueling collective bargaining.

It was once explained to me that Co-pay was very popular with negotiators for unions and management because it was easy to calculate the total cost of it for an entire self-insured corporation. If a proposed budget for the employees was known, and the budget for health benefits was agreed, the arithmetic was easy. If the company has a 20% co-pay, it can reduce the company's total insurance cost by 20%, and if it doesn't come out right, you can negotiate 18% or 22% or whatever. Late at night when these negotiations characteristically get serious, the cost of the offer and counter-offer can be quickly calculated. By contrast, if a deductible is proposed, you have to know how many people use the program, how often they would get sick per year, and even so the calculation is difficult, requiring actuaries or at least accountants. So, the explanation ran, everybody, likes co-pay, and everybody hates deductibles. The insurance people present especially like co-pay, because there will soon be a demand to add it to the package as second insurance, and the premiums for that are also easily quoted, up or down as the negotiations proceed. When it got to involve Medicare and Medicaid, the Congressmen were in essentially the same position of only wanting to know what bulk costs of the whole program would be. In short, co-pay is easy to "score". But the best that can be said for it is, it's just another short-term benefit for which long-term costs are increased because there are diminished incentives for the third-party to hold them back. Just kick the can down the road.

It has never seemed completely credible that anyone would base expensive decisions on considerations so trivial, but you never know. Having invented Medical Savings Accounts with John McClaughry in 1980, for me the mysterious resistance to high deductibles has never seemed adequately explained. Negotiators must easily see that two (or three) insurance policies will be more expensive to administer than just one. They must immediately acknowledge that being 100% insured will increase costs by making the beneficiary ignore the cost, and they are probably willing to accept (off the record) the American Actuary Association's estimate that costs are thereby increased 30%. That much alone would free up about 5% of the Gross Domestic Product since we are currently spending 18% of GDP on Health care. There has almost seemed no point to go on that wages could be increased by diverting this wasted money to the pay packet, to say nothing of the frustration many doctors feel at having no idea of the true cost of what they order, and hence little interest in making the number smaller. Obviously, if true costs are concealed, they go up. This blinding of the doctor to true costs is what makes cost-shifting easy to do without criticism. The absence of a pool of deductibles makes it impossible to generate compound interest, and that in turn makes it less practical to consider "portability" of health insurance from one employer to the next. It is at the very root of fictitious costs for medical care of all sorts, which somehow seem to the advantage of many participants in the health field. Eliminating co-pay would result in a small saving, and it probably would result in a big saving in healthcare costs. The aggregate national savings would be astonishing. Health Savings Accounts are slow to be adopted, not because they fail to save money, but because state laws have imposed mandatory insurance benefits for small-cost items, apparently passed for the main purpose of undermining deductibles.

Most people initially resist the idea of a high deductible on the ground that poor people can't afford it. When it is explained that what is intended is basically to give the poor the money to pay for it, most resistance disappears. A more correct description is that some method is constructed to give them the money, but in a way that allows them to spend money left over from healthcare, for something else they want to buy. The ability to buy something else is not the same as wasting it, and safeguards are only prudent. Retirement is the use most commonly considered. Because interest rates are being suppressed by the Federal Reserve, this proposal may be somewhat retarded for a year or two, until interest rates return to normal levels. Addition of an inflation-protection feature (like TIPS) might well enhance its attractiveness. Ultimately, the first step would be to eliminate Co-pays. Completely and permanently.

Cost to Charge Ratio (2)

of the community when all is said and done, this system is designed to keep indirect costs within reasonable boundaries. If that aggregate is spoken of as a single product, its costs can be grouped together as company-wide costs. In the case of Apple, the main costs outside direct production costs are research and development, marketing and administration. In the case of hospitals, in addition to direct production costs, there is usually less marketing cost than a manufacturer would experience and considerably more charity. By calculating the variation of prices to costs among different products, it is possible to see which particular product is carrying the burden, and which product is being subsidized. In the case of hospitals, this analysis would permit an outside opinion to form about the fairness of such cross-subsidy, which is most commonly motivated by local competition. The neighbor hospital has some expensive gizmo and we don't; we buy a gizmo to keep up with them and subsidize its cost by overcharging for everything else. Decades ago there was a rage for establishing planning commissions to determine how many gizmos a community needs, but it was largely dropped because of bickering about what is normal business flexibility in every industry. It is now generally agreed that hospitals should have the business latitude to make these choices themselves, and suffer the consequences if unrelated prices get pushed out of line by cross-subsidies of excessive expansion.Indirect costs are a much harder matter to judge. Some administrators are paid too much, some renovations are excessive, some charity is really poor debt collection; but if these things are passed off to insurance companies, who pass them off to the public, they can unduly escalate. Direct costs are whatever they are, but indirect costs are more a matter of opinion. Some insight can be gained by measuring the ratios of direct to indirect costs, and then making a national comparison of those ratios with peer institutions, a process that is hampered by the traditional regulation by states instead of nationally. Since the cost of health care has long been rising faster than the cost of living, the suspicion is fostered that insurance companies put up less price resistance than a marketplace without them would. Since the cost of major illness is often beyond the means of its victims, insurance does seem to be called for, and the higher the cost the more that is true. For more than seventy-five years, health insurance has been in the middle, between the party who wants lower prices, and the party who wants higher ones. That may well have been a bad decision, requiring some experimentation with a return toward "indemnity insurance" and away from "service benefits". That is, the insurance pays money to the patient, and the patient then pays the bill. An indemnity system protects the insurance company from cost overruns, and this at least removes the pressure for the insurance company and the hospital to collude against the patients' financial interest. Once a suspicion arises that there could be some degree of collusion between the two, it is possible to see that using insurers to police a hospital's indirect costs may be something to discourage. Alternatively, it might be possible to apply patient copayment to the indirect, but not the direct, hospital costs. At the moment, copayments have little or no effect on patient utilization, but the selective application of them might be worth at least a pilot study, to see if they could dampen prices better than they affect service volume. A copayment of 20% of the indirect cost component of a patient's bill would certainly draw attention. Even a 1% copayment would dramatize the point.

Hospital prices have been inflated far too much, and far too irregularly, to serve as cost signals. In order to minimize the true cost of charity care, the services more heavily used by the indigent have had their indirect costs minimized by cost-shifting them away to better-reimbursed departments; it is a perfectly natural thing to do. Poorly utilized departments are subsidized by better-reimbursed ones; so what else is new? To assign a fixed ratio of charges to costs would greatly hamper the flexibility needed to keep the institution from failing. But without some understood relationship between the posted, stated price and its true cost, the hospital doctors are quite unable to design a cost-effective treatment strategy. Knowing very well the lack of relationship between prices and costs, the doctors freely admit they disregard the prices entirely. While allegiance to what is scientifically best is not completely bad, it is not necessary to be so blind to the economics of the various alternatives. In time, it will lead to the design of model treatment strategies by committees. That is not itself a bad thing, except for the way it undermines individual thinking by the professional who is closest to the specifics of a case. That is a debilitating thing; a bad thing if you wish. It certainly lessens the potential for minimizing the cost of care, which is the flag it is flying. Some way must be found to improve the usefulness of prices as a guide to costs, an imperative which is otherwise certain to lead to the use of some degree of force to achieve it. And that would be a really bad thing.

from the for the Hospitals tend to be either for-profit corporations like Apple or nonprofit corporations with a different accounting system. It may help a little to know that for-profit corporations are measured by their profitability, while nonprofits are measured by the increase (or decrease) in their assets compared with last year. Items enclosed on a balance sheet with parentheses have always gone in an (unfavorable) direction. Increases (or decreases) in assets are intended to include gifts and variations in stock market prices. However, increases (or decreases) in assets like fine art don't count at all. Sometimes that can be highly misleading, as when the Barnes Art Collection increased in value by billions of dollars. Other assets, like buildings and equipment, are measured by depreciation, which is not always parallel to market prices. There is a movement favoring "mark-to-market", but investment firms are particularly opposed to marking to market, because temporary drops in market price are sometimes unrealistic, only requiring a little time to recover, a phenomenon sometimes seen in endowment funds, as well. Conventional measures of success, like the profit margin and the increase in net assets for nonprofits, are generally useful. But they can also conceal many traps. The most prominent one is to introduce these concepts when someone questions why everything costs so much as if to imply that it is unlikely that a hospital could be overcharging when it is only generating a 2% profit.

The ten dollar aspirin tablet is usually introduced at this point in the discussion, balanced by descriptions of accident room patients who try to pay nothing at all. The discussion is now one of cost-shifting. It must be obvious that the cost to charge ratio is well over a thousand percent for the aspirin, whereas Apple probably is less than a hundred percent for everything they sell you. Perhaps not, perhaps it is over a thousand percent for a number of retail items. In any event, the problem for the hospital customer is he has no way of telling what is being given free to bring the overall cost to charges down to 5%. That is, he is given no role in choosing the charity he is supporting, but he knows it varies widely between hospitals. He has to have some trust that the institution is behaving in a responsible way, which is difficult when he sees new and glistening hospital interiors or reads of seven-figure executives. Perhaps it is a little unfair to blame the trustees for avoiding embarrassing questions with no particular justification, but it does not seem unfair to ask that the hospital cost accountant prepare meaningful reports to both the management and the trustees. To the management first, to allow them time to look into oddities in the reports before having to answer for them. But no matter how it is handled, the cost accountant should be made more central than he usually is.

Every item ought to be assigned a cost to charge ratio, both inclusive and exclusive of overhead costs. It is usual to include overhead by a so-called step-down process since overhead must be paid and it generates no charges at all, only costs. But to include it in the net cost to charge ratio is potentially to bury one of the things you are trying to discover: is the overhead excessive? Having determined that point, it may be legitimate to re-include overhead in the "net" calculation of the cost to charges. Hence the suggestion of reporting it both ways. No one doubts the books balance; the items of expenditure include most of the costs. The essential issue is whether this is all pretty expedient, whether too much frivolous expenditure is being permitted by shifting its cost to certain profit centers. When this cost to charge system is compared among other hospitals or other years in the same hospital, it is possible to recognize the unusual items or departments quickly. However, the beginning trustee or utilization reviewer may need to have the costs and charges stripped out and aggregated, to highlight the highly deviant figures for ready appraisal. Consequently, it may be necessary for the insurance company to require reports of certain items, structured in that way. Other such reports may be needed to identify overpaid employees, or overstaffed departments, usually as patients and dollars per employee, compared with other institutions. Ultimately, it may even be necessary to establish norms, but that begins to resemble micromanaged cost control, when peer pressure may be all that is required.

Executive Summary, continued

continues the inequity of denying the same tax exemption to everyone because of the nature of employment, and would be very hard to defend in open public debate, but even equalization will fail to adjust historical disparities in premiums upon transition to universal coverage (because of resistance to rebalancing the pay-packets). Secondly, service benefit compromises which might be tolerated in a private system become dubious within a government mandated one. And thirdly, businesses have outgrown their 20th Century role as a rescuer of vital community service, and now often regard health costs as a growing burden to company competitiveness, which stockholders must be induced to accept. Businesses themselves may be changing perspective and beginning to see the advantages of employee-selected and employee-owned portable health insurance. They may have come to see that employer-basing drove them toward selecting a one-year term model, rather than a lifetime whole-life model, and the employee-owned model is portable between jobs, and able to pay much of its own cost by compounding investment income. Many of the present complaints grow from discontinuity, while continuous coverage greatly reduces the expensive patchwork of multiple insurance forms, pre-existing conditions, uncoordinated successive insurance plans -- and is able to generate investment income, besides. The easiest way to become adjusted to a billing and information system is to avoid frequent changes in the companies running them. Forcing insurance companies to maintain a nationally uniform system is a disruptive way to get there, reduces innovation and competition. Beyond a certain point, people will rebel.

But among the opportunities neglected by mandated universal-coverage at community-rated seem to be: Opportunities for coordinated compound interest to finance coordinated lifetime systems; opportunity to coordinate insurance company information barriers at least enough to eliminate the need for up to three insurance forms to pay for one medical service completely; an opportunity to re-examine the technicalities of traditional patient cost-sharing, thereby downgrading or eliminating ineffective co-pay, but expanding much preferable deductibles buffered by Health Savings Accounts. In the past, many compromises were made to accommodate the highly untraditional insurance concept of service benefits, including bungled but laudable transitions to reimbursement by diagnosis-related groupings. It would be a great mistake, however, to equate this hospital approach with system-wide elimination of fee-for-service. Information systems and cost accounting based on item charges are highly developed and cumbersome to replace; no system outside the acute care hospital has more than experimented with other approaches. It would seem far simpler to modify insurance design to isolate two billing approaches (itemization and capitation) and force them to include, side by side, both office-based care and inpatient services using the same hospital cost accounting data to establish reimbursements. Mandated universal systems can facilitate some of these things, but the real test of democracy is to achieve them without resorting to force.

All of the foregoing areas of omission from the Affordable Care Act should be regarded as areas where improvements in the health administrative system might be possible for either political party to espouse. Therefore, if both parties might agree on some of them, progress might continue even though there is another acrimony in the background. The list of other approaches opened up to examine is probably longer than the average reader has the patience to read, but it includes Last-year of Life escrow, and gradual dispersal of the physical centers of health delivery away from tertiary centers, not toward them. More modest goals and timetables for computerizing physician notes would greatly reduce transition costs for providers. Centralized statistics might thereby be lessened, but the quality of care need not be. The savings from digitizing physician office notes have been greatly overstated, and mostly apply to physician practice aggregates, which inherently magnify communication and record-keeping costs.

Although health reform is now portrayed as a settled decision, the debate which preceded it never anticipated a 50% swing in cost difference between Obamacare and its insurance alternatives. At this time of national financial turmoil, such savings might actually exceed 5% of Gross Domestic Product, thus providing appreciable funds for other urgencies. It seems incredible that such an equilibrium would escape re-examination.

PRIORITIES NOT EXPLORED: Every reformer must choose priorities, but cannot escape criticism for other roads not taken. The chosen highest priority of ensuring everyone with community-wide premiums must also now demonstrate it was achievable without injuring the quality of care. It must also be demonstrated that the commendable goal of spreading expenses widely did not require so much complexity and inflexibility that the delivery system could not keep up with scientific advances. Even if all that can be achieved, the question will remain whether the time and effort might have been better applied to solve a myriad of other healthcare problems which have less to do with insurance. Other problems undiscussed in this paper might have included the financial abandonment of inpatient psychiatry, the unnecessary diversion of non-emergencies into hospital accident rooms in order to retain control of the system within acute care hospitals, unprioritized expenses encouraged by internal hospital cost-shifting, and distorted state budgets encouraged by complex shifting of underfunded hospital Medicaid costs to other payers, especially Medicare. By burying medical costs within insurance, physicians directed to use less expensive methods are denied truly useful information about the cost of components. (That is, not about posted charges, but about what is the true cost.) Item costs are the central signals used, and the present attack on the fee for service offers no substitute signals. The nursing profession is distracted by clerical functions, and its training programs transferred out of hospitals into less meaningful college environments, by reimbursement bundling. The medical profession has seen its overhead costs inflated by compliance with questionable reimbursement requirements, effectively impoverishing primary care, and overcompensating procedural alternatives which can more easily transfer overhead to the hospital. The serious issue of "Job Lock" raised by the earlier Clinton proposal is an inherent component of employer basing, probably continuing as long as employer basing does, and possibly as long as the Tenth Amendment does. The tax inequities for self-employed and small-business employed persons are stubbornly continued, as will be exposed when premiums stabilize. Many of these issues have insurance features because insurance is the dominant method of payment, but they are not considered here as direct consequences of the insurance model. While this list could be extended, its present extent already strains the limits of what can be coherently grouped by sources and causes. This paper confines a critical analysis of those insurance issues where solutions are proposed.

and Generally empowers non-physician administrative control through reimbursement as a means to control rather than assist the higher goal of widespread good medical care.Introduction, continued

Almost three years after the President presented 2500 pages of the proposed health law to Congress for approval, the commentary is hampered because important rules are still unissued. If the program eventually works well, criticism and proposed alternatives may well be set aside. But if enough voters become upset during the early stages of implementation, there will be no escape from the review of other options. To some people alternatives of any sort would seem premature, but here they grow from a preliminary perception that this enormous program has wandered from identifying the basic problem, and thus failed to concentrate on a coherent remedy for solving it.

At its root, the Affordable Care Act is, quite rightly, an insurance reform. Reform of a system is considered to be failing because healthcare costs were rising alarmingly and many citizens had no insurance to buffer them from it. The bulk of citizens did have insurance, and their indifference to cost was considered a cause of the escalation. It was therefore elected to make health insurance universally mandatory and uniform, with government subsidies for those who could not afford it. A unified system would eliminate enough inefficiency to pay for itself, and while some individuals would see higher costs, average lifetime health costs would decline overall, as the peaks and valleys of lifetime costs level out. Governmental control of the insurance system would thereby put it in a position to ignore the nationwide indifference to costs, while its evident power to ration would make rationing unnecessary. More than this was, of course, promised during political campaigns, and more were probably secretly hoped for. But this short summary intends to make the best case for what was offered and will be accepted as the basis for analysis in this paper. If less than the best case makes an appearance, it will be noticed.

Insurance reform is expected to change something, so it seems fair to criticize the Affordable Care Act for accepting three major questionable aspects of the old system, as well as two innovations of its own. Much of this critique will focus on the new problems making the old problems worse, possibly bringing other old problems to the surface, as well. Criticism without offering a substitute is useless, so this paper re-examines Health Savings Accounts in this new environment and finds it actually makes that alternative more attractive. Combined with a repeal of the present tax preference for employer-controlled coverage, these two reforms might be sufficient alternative, with a more gradual beginning. However, the reader is asked to consider the far more ambitious proposal for lifetime, individually owned health policies, universally mandated if you please, with the potential for internally generated investment income to pay for substantial parts of its cost. And the reader is asked to look beyond insurance reform as the way to reduce medical costs without rationing, with the example of moving the center of medical care (physician offices) away from the acute care hospital campus, toward the concentrations of most illness (retirement villages). This latter would largely consist of removing obstacles to where the system seemingly wants to go, anyway. Several other non-insurance reforms are presented in sketchy form, with the urging that most of their seemingly insurance-related features are merely a reflection of present predominant payment routing through insurance, a feature now found in almost anything medical. When they rise to a level embedded in law, they may, of course, require legislative attention to reverse them.

The difficulties it should first correct are distortions of medical care imposed by existing insurance-like financing, searching for a way to conduct a pre-payment system. High costs and failure to include everyone are important issues. But they were only two of many distortions emerging from an employer-based, tax-preferenced, prepayment system. It had been awkwardly forced into an ill-suited term-insurance format long before the present Administration took office. The national clamor of dissatisfaction did not originate out of a united voice of the uninsured population demanding more free coverage, nor was individual cost constraints a central problem for the insured public; rather, clamor mostly originated with third-parties imagining that soaring aggregate costs could be constrained by cost-shifting them, and actuaries endorsing the delusion. Fundamental sources of unrest are to be found in limitations of one-year term insurance itself when applied to a pre-payment process for lifetime expenses -- further complicated by accidentally employer-basing it. Both of these distortions were seriously amplified by uneven bestowal of tax preference, also by accident. The number of small claims is too large to support the claims-processing cost. The size of the premium pool is too small to permit so much free care to be hidden within it because the average premium must not preclude the middle class from affording it. The cost of young and old dependents is rising, the cost of the employee who pays the bill is shrinking, but they are mostly the same people at different ages. The result was unaffordable delivery cost throughout a century of progressively vanishing disease. The health beneficiaries of this process were the patients, with longevity increased by three decades. The financial beneficiaries are also easy to identify. Just count the growing number of non-professionals who are making a living serving it.